The life of a small business owner is not easy! Luckily, the Government has a similar opinion. Many benefits are provided both by the Central and State Governments to promote the growth of small-scale businesses like yours.

#15 Best Government Subsidy List For Small Business like yours in India

1. The Credit Guarantee Fund Scheme (CGTMSE) for MSMEs

- Only Micro & Small Enterprises as per the MSMED Act are eligible.

- Both the Manufacturing and Service sectors covered.

- Under this business subsidy scheme, you can get loans of up to Rs. 100 lakhs.

- No collateral deposit required.

- Both Term Loans & Working Capital Loans are offered under this scheme.

- No third party guarantees required.

- Both existing and new enterprises are eligible for loans under this scheme.

- Having IT PAN number is compulsory to avail this loan.

Benefits you get from this scheme: Loan Amount and Capital Subsidy

✔ You can apply for loans without collateral deposits.

✔ Third-party guarantees not required.

✔ If you fail to repay the loan, this scheme will cover your lender a certain percentage of the loan taken.

✔ If you’ve taken a loan up to 5 lakhs – 85% of your loan will be covered.

✔ For loans between Rs 10 lakh to Rs 100 lakh (for retail activity only) – 50% of your loan will be covered. If the small business is owned by women, then 80% will be covered.

How to register and apply for a loan under CGTMSE

Step 1 – Form the Business Organization

Register your business -> Obtain the necessary licenses and permissions from the respective Govt. authority -> Open a current bank account -> Apply for business PAN Card.

Step 2 – Prepare the Project Report or Business Plan

Submit a full-proof project report with market analysis, ROI, Break-Even and Payback calculations.

Step 3 – Apply for the sanction of Bank Loan

Apply for the loan ->Talk with at least 2 to 3 banks that are nearby you.

Step 4 – Get Coverage under CGTMSE Scheme

After getting the sanction of the loan, the bank will apply for the subsidy to the CGTMSE organization. After the approval, you have to pay the CGTMSE guarantee and service fee if any.

List of Banks Who Provide Subsidized Loans under CGTMSE Scheme

- Public Sector Banks (21 nos.)

- 1 Allahabad Bank

- 2 Andhra Bank

- 3 Bank of Baroda

- 4 Bank of India

- 5 Bank of Maharashtra

- 6 Bharatiya Mahila Bank Ltd.

- 7 Canara Bank

- 8 Central Bank of India

- 9 Corporation Bank

- 10 Dena Bank

- 11 IDBI Bank Limited

- 12 Indian Bank

- 13 Indian Overseas Bank

- 14 Oriental Bank of Commerce

- 15 Punjab & Sind Bank

- 16 Punjab National Bank

- 17 Syndicate Bank

- 18 UCO Bank

- 19 Union Bank of India

- 20 United Bank of India

- 21 Vijaya Bank

SBI & Its Associates Banks (6 nos.)

- 1 State Bank of India

- 2 State Bank of Bikaner & Jaipur

- 3 State Bank of Hyderabad

- 4 State Bank of Mysore

- 5 State Bank of Patiala

- 6 State Bank of Travancore

Private Sector Banks (21 nos.)

- 1 Axis Bank Ltd.

- 2 Catholic Syrian Bank Ltd.

- 3 City Union Bank

- 4 Development Credit Bank Ltd.

- 5 HDFC Bank Ltd.

- 6 ICICI Bank Ltd.

- 7 IDFC Bank Ltd.

- 8 IndusInd Bank Ltd.

- 9 ING Vysya Bank Ltd.

- 10 Karnataka Bank Ltd.

- 11 Kotak Mahindra Bank Ltd.

- 12 Lakshmi Vilas Bank Ltd.

- 13 Tamilnad Mercantile Bank Ltd.

- 14 The Dhanalakshmi Bank Ltd.

- 15 The Federal Bank Ltd.

- 16 The Jammu & Kashmir Bank Ltd.

- 17 The Karur Vysya Bank Ltd.

- 18 The Nainital Bank Ltd.

- 19 The Ratnakar Bank Ltd.

- 20 The South Indian Bank Ltd.

- 21 YES Bank Limited

Foreign Banks (4 nos.)

- 1 Barclays Bank PLC

- 2 Bank of Bahrain and Kuwait

- 3 Deutsche Bank

- 4 Standard Chartered Bank

Regional Rural Banks (66 nos.)

- 1 Allahabad UP Gramin Bank

- 2 Andhra Pradesh Grameena Vikas Bank

- 3 Andhra Pragathi Grameena Bank

- 4 Aryavart Gramin Bank

- 5 Assam Gramin Vikash Bank

- 6 Baitarani Gramya Bank

- 7 Ballia Etawah Gramin Bank

- 8 Bangiya Gramin Vikash Bank

- 9 Baroda Gujarat Gramin Bank

- 10 Baroda Rajasthan Gramin Bank

- 11 Baroda Uttar Pradesh Gramin Bank

- 12 Bihar Kshetriya Gramin Bank

- 13 Chaitanya Godavari Grameena Bank

- 14 Chattisgarh Rajya Gramin Bank

- 15 Dena Gujarat Gramin Bank

- 16 Hadoti Kshetriya Gramin Bank

- 17 Himachal Gramin Bank

- 18 Jaipur Thar Gramin Bank

- 19 Jammu & Kashmir Gramin Bank

- 20 Jharkhand Gramin Bank

- 21 Karnataka Vikas Grameena Bank

- 22 Kashi Gomti Samyut Gramin Bank

- 23 Kaveri Grameena Bank

- 24 Kerala Gramin Bank

- 25 Langpi Dehangi Rural Bank

- 26 Madhya Bharat Gramin Bank

- 27 Madhya Bihar Gramin Bank

- 28 Maharashtra Godavari Gramin Bank

- 29 Maharashtra Gramin Bank

- 30 Malwa Gramin Bank

- 31 Meghalaya Rural Bank

- 32 MGB Gramin Bank

- 33 Mizoram Rural Bank

- 34 Nainital – Almora Kshetriya Gramin Bank

- 35 Narmada Malwa Gramin Bank

- 36 Neelachal Gramya Bank

- 37 Pallavan Gramin Bank

- 38 Pandyan Grama Bank

- 39 Parvatiya Gramin Bank

- 40 Pragathi Krishna Grameena Bank

- 41 Prathama Bank

- 42 Puduvai Bharathiar Grama Bank

- 43 Punjab Gramin Bank

- 44 Purvanchal Gramin Bank

- 45 Rajasthan Gramin Bank

- 46 Rewa Siddhi Gramin Bank

- 47 Rushikulya Gramya Bank

- 48 Samastipur Kshetriya Gramin Bank

- 49 Saptagiri Grameena Bank

- 50 Sarva Haryana Gramin Bank

- 51 Sarva UP Gramin Bank

- 52 Satpura Narmada Kshetriya Gramin Bank

- 53 Saurashtra Gramin Bank

- 54 Sharda Gramin Bank

- 55 Shreyas Gramin Bank

- 56 Sutlej Gramin Bank (SGB)

- 57 Telangana Gramin Bank

- 58 Tripura Gramin Bank

- 59 Triveni Kshetriya Gramin Bank

- 60 Uttar Bihar Gramin Bank

- 61 Uttaranchal Gramin Bank

- 62 Uttarbanga Kshetriya Gramin Bank

- 63 Vananchal Gramin Bank

- 64 Vidharbha Kshetriya Gramin Bank

- 65 Vidisha Bhopal Kshetriya Gramin Bank

- 66 Wainganga Krishna Gramin Bank

For more details about this scheme – Click here

#2. Government Subsidy For Organic Farming

- Individuals, a group of farmers/growers, proprietary, and partnership firms, Co-operatives, Fertilizer industries, Companies, Corporations, and NGOs are eligible to get the subsidy for biofertilizer and biopesticide manufacturing operation.

- APMCs, Municipalities, NGOs and Private entrepreneurs are eligible to get the subsidy for fruit and vegetables waste compost unit.

- Azotobacter, Rhizobium, PSB, Azospirillum, Acetobacter, Trichoderma, and Mycorrhiza are some of the profitable products, you can start manufacturing under this scheme.

The major objectives of the scheme are

- To promote organic farming in the country by making available organic inputs such as biofertilizers, Biopesticides, and fruit & vegetable market waste compost.

- To increase agricultural productivity while maintaining soil health and environmental safety.

- To reduce the total dependence on chemical fertilizers and pesticides by increasing the availability and improving the quality of biofertilizers, biopesticides, and composts in the country.

- To convert organic waste into plant nutrient resources.

- To prevent pollution and environment degradation by proper conversion and utilization of organic waste.

For more details about this scheme – Click here

#3. Technology Upgradation Fund Scheme (TUFS) For Textile Industry

- The Ministry of Textile launched this business subsidy Scheme to help the textile entrepreneurs in India.

- Basically, the scheme has a provision of a one-time capital subsidy for eligible benchmarked machinery at the rate of 15%.

- The subsidy is for garments and technical textiles segments with a cap of Rs. 30 crores.

- In addition, one can avail the subsidy at the rate of 10% for weaving, processing, jute, silk and handloom segments with a cap of Rs. 20 crores.

- Reimbursement of 5% on the interest charged by the lending agency on a project of technology up gradation in conformity with the Scheme.

- In weaving – (i) 6% Interest Reimbursement (IR) and 15% Capital Subsidy (CS) on brand new shuttleless looms or 30% Margin Money Subsidy (MMS) for power loom sector. (ii) 2% IR or 8% MMS on second hand imported shuttleless looms with 10 years vintage and with a residual life of 10 years; (iii) for 30% MMS- the capital ceiling of Rs. 5 crores and subsidy cap of Rs. 1.5 crore would be adhered to encourage adequate investment by MSME sector.

- Cover for foreign exchange rate fluctuation / forward cover premium not exceeding 5% for all segments except for new stand alone / replacement/modernization of spinning machinery for which the foreign exchange rate fluctuation/forward cover premium will be 2%.

- An option to MSME textile and jute sector to avail of 15% Margin Money subsidy instead of 5% interest reimbursement on investment in TUF compatible specified machinery subject ceiling on margin money subsidy of Rs. 75 lakh.

- 5% interest reimbursement plus 10% capital subsidy for specified processing, garments and technical textile machinery.

- Interest subsidy/capital subsidy / Margin Money subsidy on the basic value of the machinery excluding the tax component for the purpose of valuation.

- 30% capital subsidy instead of 5% interest reimbursement on benchmarked machinery of the silk sector as applicable for the Handloom sector.

- The Scheme will cover only automatic shuttleless looms of 10 years vintage and with a residual life of minimum 10 years.

- Investments like factory building, pre-operative expenses and margin money for working capital are eligible for benefit of reimbursement under the Scheme meant for the apparel sector and handloom with a 50% cap.

- Interest reimbursement period is 7 years including implementation/moratorium period.

For more details about this scheme – Click here

#4. Scheme for Technology Upgradation/ Establishment/ Modernization for Food Processing Industries

- This government scheme covers the following activities: Setting up/expansion/modernization of food processing industries covering all segments viz fruits & vegetables, milk products, meat, poultry, fishery, oilseeds and such other agri-horticultural sectors leading to value addition and shelf life enhancement including food flavours and colours, oleoresins, spices, coconut, mushroom, hops.

- The assistance is in the form of grant subject to 25% of the plant & machinery and technical civil works subject to a maximum of Rs. 50 lakh in General Areas and 33.33% up to Rs. 75 lakh in Difficult Areas.

For more details about this scheme – Click here

#5. Integrated Development of Leather Sector – Scheme for Leather Industry

- The government scheme is open to all existing units in the Footwear, Leather and other accessories including tanneries, saddlery, leather goods, leather footwear, footwear component sector and non-leather footwear.

- The units should have a cash profit for 2 years.

- They also should be continuously undertaking successful and bankable programs on technology up-grading on or after January 1, 2016.

- The scheme is also open to new units provided they meet certain criteria.

- The new units seeking assistance under the Integrated Development of Leather scheme would be considered only if the project is evaluated and appraised. It should be found to be bankable and viable by the bank that will be providing the GOI assistance.

- In case the units are capable of self-financing, then the project viability will be done based on the strength of the working-capital of such units.

For more details about this scheme – Click here

#6. Credit Linked Capital Subsidy loan Scheme (CLCSS) for Technology Upgradation

- To help SMEs flourish in international trade markets, the Ministry of Small Scale Industries (SSI) runs a scheme for technology up gradation of Small Scale Industries.

- It aims at facilitating technology upgradation by providing upfront capital subsidy of 15% (limited to a maximum of Rs.15 lakhs) to SSI units for credit availed by them for the modernization of their plant and machinery.

- All sole proprietorships, partnership firms, cooperative, private and public limited companies are eligible for this scheme.

Who are eligible?

✔ Indian Institutes of Technology (IITs).

✔ National Institutes of Technology ( NITs).

✔ Engineering Colleges.

✔ Technology Development Centres, Tool Rooms, etc.

✔ Other recognized R&D&/or Technical Institutes/Centres, Development Institutes of DIP&P in the field of Paper, Rubber, Machine Tools, etc.

✔ Biotech Industry

✔ Common Effluent Treatment Plant

✔ Corrugated Boxes

✔ Drugs and Pharmaceuticals

✔ Dyes and Intermediates

✔ Industry based on Medicinal and Aromatic plants

✔ Plastic Moulded/ Extruded Products and Parts/ Components

✔ Rubber Processing including Cycle/Rickshaw Tyres

✔ Food Processing (including Ice cream manufacturing)

✔ Poultry Hatchery & Cattle Feed Industry

✔ Dimensional Stone Industry (excluding Quarrying and Mining)

✔ Glass and Ceramic Items including Tiles

✔ Leather and Leather products including Footwear and Garments

✔ Electronic equipment viz tests, measuring and assembly/ manufacturing, industrial process control, analytical, medical, electronic consumer and communication equipment, etc.

✔ Fans and Motors Industry

✔ General Light Service (GLS) Lamps

✔ Information Technology (Hardware)

✔ Mineral-Filled Sheathed Heating Elements

✔ Transformer/ Electrical Stampings/ Laminations/ Coils/ Chokes including Solenoid Coils

✔ Wires and Cable Industry

✔ Auto parts and components

✔ Bicycle Parts

✔ Combustion Devices/ Appliances

✔ Forging and Hand Tools

✔ Foundries – Steel and Cast Iron

✔ General Engineering Works

✔ Gold Plating and Jewellery

✔ Locks

✔ Steel Furniture

✔ Toys

✔ Non-Ferrous Foundry

✔ Sport Goods

✔ Cosmetics

✔ Ready mate Garments.

✔ Wooden Furniture

✔ Mineral Water Bottle

✔ Paints, Varnishes, Alkyds and Alkyd Products

✔ Agricultural Implements and Post Harvest Equipment

✔ Beneficiation of Graphite and Phosphate

✔ Khadi and Village Industries

✔ Coir and Coir Products

✔ Steel Furniture

✔ Toys

✔ Non-Ferrous Foundry

✔ Sports Goods

✔ Cosmetics

✔ Ready-made Garments

✔ Wooden Furniture

✔ Mineral Water Bottle

✔ Paints, Varnishes, Alkyds and Alkyd Products

✔ Agricultural Implements and Post Harvest Equipment

✔ Beneficiation of Graphic and Phosphate

✔ Khadi and Village Industries

✔ Coir and Coir Products

✔ Steel Re-rolling and Pencil Ingot making Industries

✔ Zinc Sulphate

✔ Welding Electrodes

✔ Sewing Machine Industry

Benefits you get from this scheme: Loan Amount and Capital Subsidy

✔ The scheme provides an upfront capital subsidy of 15% to MSEs, including tiny, khadi, village, and coir industrial units, on institutional finance of up to Rs 1 crore availed by them, for induction of well-established and improved technology in the approved 51 sub-sectors/products.

✔ A maximum of Rs 1 crore with the rate of subsidy of 15% is offered under this scheme.

How to register and apply for a loan under CLCS

✔ Visit the official website of the MSME department:

#7. Market Development Assistance Scheme for Micro, Small & Medium Enterprises

- The scheme offers to fund for participation by manufacturing Small & Micro Enterprises in International Trade Fairs/ Exhibitions under MSME India stall.

- The objective of this loan scheme is to encourage small and micro exporters in their efforts at tapping and developing overseas market.

#8. Technology & Quality Upgradation Support for MSMEs

- In an effort to increase the adoption of quality standards by the MSME sector of India, Government provides this loan subsidy.

- Basically, this is for acquiring ISO certifications like ISO 9000, ISO 14001 and HACCP.

- Also, it aims to expand the domestic and global market share of Indian MSME products.

- This scheme focuses on the two important aspects, namely, enhancing the competitiveness of the MSME sector through Energy Efficiency and Product Quality Certification.

- The second objective is to improve the product quality of MSMEs and to encourage them towards becoming globally competitive

For more details about this scheme – Click here

#9. Mini Tools Room and Training Centre Scheme

- Here, the Govt. wants to provide technical support to the MSMEs and training facility in tool manufacturing and tool design to create a workforce of skilled workers, supervisors, engineers/designers, etc.

- The objectives of the Mini Tool Room & Training Centres would be-

To manufacture Jigs, fixtures cutting tools, gauges, press tools, plastic moulds, forging dies, pressure casting dies and other toolings for Small Scale Industries.

✔ Advanced tool making process using CAD/CAM techniques are to be adopted.

✔ To provide training facility in tool manufacturing and tool design to generate a workforce of skilled workers, supervisors, engineers/designers etc.

✔ To work as a Nucleus Centre for providing Consultancy, information service, documentation etc, for solving the problems related to toolings of industries in the region.

✔ To act as a common facility Centre for small scale industries and to assist them in product and prototype development.

#10. Government Loan Subsidy for Small Business from NSIC

- NSIC provides two basic subsidies. Raw material assistance and marketing assistance.

Raw Material Assistance Scheme aims at helping Small Scale Industries/Enterprises by way of financing the purchase of Raw Material (both indigenous & imported). This gives an opportunity for SSI to focus better on manufacturing quality products.

Marketing support is provided to Micro, Small & Medium Enterprises through National Small Industries Corporation (NSIC) to enhance competitiveness and marketability of their products.

For more details about this scheme – Click here

#11. Government Loan Subsidy for Small Business for Cold Chain

- Individual, Groups of Entrepreneurs, Cooperative Societies, Self Help Groups(SHGs), Farmers Producer Organizations (FPOs), NGOs, Central/State PSUs etc. with a business interest in Cold Chain solutions are eligible to set up an integrated cold chain and preservation infrastructure and avail grant under the Scheme

- First of all, the applicant must have a sound financial background. You must have a Net worth more than 1.5 times of the grant applied for.

- The objective of the scheme of Cold Chain, Value Addition and Preservation Infrastructure is to provide integrated cold chain and preservation infrastructure facilities without any break from the farm gate to the consumer.

- It covers pre-cooling facilities at production sites, reefer vans, mobile cooling units as well as value addition centres.

- Basically, the centres that include infrastructural facilities like Processing/Multi-line Processing/ Collection Centres, etc. for horticulture, organic produce, marine, dairy, meat, and poultry etc.

For more details about this scheme – Click here

#12. Under Technology Mission on Coconut (TMOC) For Coconut Producing Units

- Any individual can avail the assistance for setting up of coconut-based industry other than the husk.

- Technology for the different products is available with the board on payment of technology transfer fee. The product list includes virgin coconut oil and dietary fibre, packing of tender coconut water, spray dried milk powder, vinegar, and other convenience foods.

For more details about this scheme – Click here

#13. SAMPADA Scheme for Agro-Marine Produce Processing

- SAMPADA stands for Scheme for Agro-Marine Produce Processing and Development of Agro-Processing Clusters.

- With a budget of Rs. 6000 Crores, the SAMPADA scheme is aimed to integrate current and new schemes in the food processing sector.

- The main objective is reducing food wastage and doubling farmers’ income.

- Also, it includes new schemes like Infrastructure for Agro-processing Clusters, Creation of Backward and Forward Linkages, Creation / Expansion of Food Processing & Preservation Capacities.

- SAMPADA is a comprehensive package to give a renewed thrust to the food processing sector in the country.

- It aims at the development of modern infrastructure to encourage entrepreneurs to set up food processing units based on cluster approach.

- It provides effective and seamless backward and forward integration for processed food industry by plugging gaps in supply chain and the creation of processing and preservation capacities and modernization/ expansion of existing food processing units.

- The implementation of SAMPADA will result in the creation of modern infrastructure with efficient supply chain management from farm gate to the retail outlet.

- It will not only provide a big boost to the growth of food processing sector in the country but also help in providing better prices to farmers and is a big step towards doubling of farmers’ income.

- It will create huge employment opportunities, especially in the rural areas.

- It will also help in reducing wastage of agricultural produce, increasing the processing level. Additionally, customers can expect the availability of safe and convenient processed foods at an affordable price.

For more details about this scheme – Click here

#14. Government Loan Subsidy for Small Business – Dairy Farming

- In an effort to further strengthen the dairy farming industry in India, the NABARD dairy farming subsidy was launched.

- In addition to milk, the manure from animals provides a good source of organic matter for improving soil fertility and crop yields.

- The gobar gas from the dung is used as fuel for domestic purposes as also for running engines for drawing water from well.

- The surplus fodder and agricultural by-products are gainfully utilized for feeding the animals.

For more details about this scheme – Click here

#15. Government Loan Subsidy for Small Business for Horticulture

- National Horticulture Board (NHB) was set up by the Government of India in 1984.

- Basically, it is an autonomous society under the Societies Registration Act 1860.

- The objectives of the National Horticulture Board are the development of hi-tech commercial horticulture, development of modern post-harvest management infrastructure, promotion, market development of fresh horticultural produce and more.

For more details about this scheme – Click here

# 9 Trusted Business Loan for Women Entrepreneurs in India

To facilitate the growth of Women Various Business Loans for women enterpreneurs in india offered exclusively to promote women entrepreneurship. Business Loans are the need of every single entrepreneur. There are over 8 million women entrepreneurs in India, with Tamil Nadu having the highest share.

The role of women has changed drastically in the past few years for the better. A lot of women are entering the business to earn bigger and better. India needs more Women Entrepreneurs to grow economically, socially and culturally. Women constitute around half the total (48%) Indian population but their participation in the economic activities is only 25%. To facilitate this growth, better access to finance has been offered especially for women in India.

Here is a list of various small business loans offered exclusively for women to promote women entrepreneurship.

1. Loan Under Annapurna Scheme

✔ This business loan Offered by State Bank of Mysore.

✔ Available for women who’re setting up the food catering industry in order to sell packed meals, snacks, etc.

✔ The loan amount must be used to buy utensils and other kitchen tools and equipment.

✔ Under this business loan, you must pledge the assets of your business as collateral security along with a personal assurance from a guarantor.

✔ You will get up to a maximum amount of ₹50,000 which has to re-paid in monthly installments for 36 months.

✔ You don’t have to pay EMI for the first month.

✔ But the interest rate depends upon the market.

2. Stree Shakti Package For Women Entrepreneurs in India

✔ Stree Shakti Business Loan Offered by most of the SBI branches to women entrepreneurs who have at least 50% share in the ownership of a firm or business.

✔ Also, you should have taken part in the state agencies run Entrepreneurship Development Programmes (EDP).

✔ If the Business loan amount is more than ₹2 lakhs, the interest will be reduced by 0.50%.

3. Bharatiya Mahila Bank Business Loan

✔ As Women entrepreneur you can claim for Business Loan up to ₹20 crores in this scheme. This Business loan will be given against property.

✔ This is a Business loan for women entrepreneurs looking to start new ventures in the fields of the retail sector, manufacturing industries.

✔ But there is no requirement of collateral security for this Business loan of up to ₹1 crore.

4. Business Loan Under Dena Shakti Scheme

✔ Offered by Dena bank to those women entrepreneurs in the fields of like agriculture, manufacturing, micro-credit, retail stores, or small enterprises.

✔ So a maximum Business loan of ₹20 lakhs for retail trade will be given to you under this scheme.

5. Business Loan Under Udyogini Scheme

✔ Offered by Punjab and Sind Bank to provide women entrepreneurs involved in like agriculture, retail, and small business enterprises.

✔ This Business loan has flexible terms and concessional interest rates.

✔ So the maximum amount of Business loan under this scheme for women is ₹1 lakh, if the age bracket is 18-45 years

6. Business Loan Under Cent Kalyani Scheme

✔ This Business loan Offered by the Central Bank of India with the aim of supporting women in starting a new business or expand an existing one.

✔ This Business loan can be availed by you if you are involved in village and cottage industries, Like micro, small and medium enterprises, self-employed women, agriculture and allied activities, retail trade, and government-sponsored programs.

✔ No collateral security required, no guarantor needed, no processing fees.

✔ The maximum Business loan that can be granted under the scheme is Rs. 100 lakhs.

7. Women Entrepreneur Loan Under Mahila Udyam Nidhi Scheme

✔ This Business loan scheme is launched by Punjab National Bank and aims at supporting the women entrepreneurs involved in the small scale industries.

✔ These Business loans can be repaid over a period of 10 years.

✔ There are different plans for beauty parlors, daycare centers, purchase of auto-rickshaws, two-wheelers, cars, etc.

✔ The maximum amount granted under this scheme is ₹10 lakhs.

✔ Interest depends upon the market rates.

8. Loan Under Mudra Yojana Scheme For Women Entrepreneur

✔ This scheme is launched by the Govt. of India for individual women wanting to start small new enterprises and businesses like beauty parlors, tailoring units, tuition centers, etc. as well as a group of women wanting to start a venture together.

✔ So No collateral needed.

Under this GOVT scheme, capital loans are provided to finance micro-business operating in the manufacturing, trading and service sector. If you’re a very small business or a startup having nothing to start off with, this is for you. Low-cost capital new business Loans are approved and given by public sector banks, private sector banks, co-operative societies, small banks, scheduled commercial banks and rural banks.

There are 3 schemes under this Yojana–

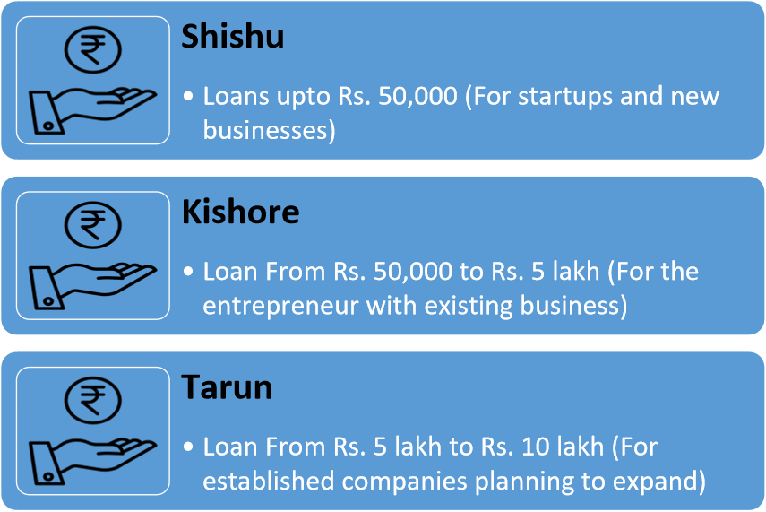

- Shishu – Business loan amount is limited to ₹50,000 for businesses that are in their initial stages.

- Kishor – Business loan amount ranges between ₹50,000 and ₹5 lakhs for the well-established enterprise.

- Tarun – Business loan amount is ₹10 lakhs for purpose of expanding the business.

Features of Pradhan Mantri Mudra Yojana

| Interest Rate | Depends on business requirements varies from bank to bank. Generally range between 7% -12% interest rate. |

| Loan Amount | Up to ₹ 50,000 under the Shishu Loan categoryFrom ₹ 50,000 to ₹ 5 Lakh under the Kishor Loan categoryFrom ₹ 5 Lakh to ₹ 10 Lakh under the Tarun Loan category |

| Mudra Loan Age Limit | 18 to 65 years |

| Processing Fee | NIL under Kishor and Shishu schemes.0.5% for Tarun loan |

| Loan Repayment Period | From 3 years to 5 years |

| Maximum Loan Amount | Up to Rs. 10 lakh |

| Collateral/Security | Not required |

Mudra Loan Other Details:

# Products offered under Mudra Loan

Under this scheme of PMMY, you have three different schemes to choose from according to the needs of your business, namely ‘Shishu’, ‘Kishore’, and ‘Tarun’ which are meant for the development and financing of beneficiary micro-units or entrepreneurs.

Mainly for the Purpose of which Mudra Loan can be used

Mudra loan scheme helps MSMEs in the following Purpose:

- Starting a Product and Service business

- Business expansion

- Purchase of plant and machinery

- To get working capital for the business

- Purchasing equipment or commercial vehicle

- Hiring or training employees

Mudra Loan Documents Required

Documents required for availing of a Mudra Loan are:

- Self-written business Plan

- Duly filled application form of Mudra Yojana

- 2 recent passport size photos of the applicant

- Identity Proof: Aadhaar Card, Valid Passport, Voter ID Card, Valid Driving License, and PAN Card.

- Residence Proof: Utility bill, Aadhaar card, Passport, Voter’s ID, Bank passbook

- Proof of belonging to a special category, such as SC, ST, OBC, Minority, etc. (if applicable)

- Last 6 months bank account statement.

- Proof of business existence: Certificate, License, registration, or any other documents confirming the business existence, address, and ownership.

- Any other documents required by the bank

How to Apply for Mudra Loans?

There are many banks, such as Allahabad Bank, Axis Bank, Bank of Baroda, Bank of India, Canara Bank, Central Bank of India, IDBI Bank, HDFC Bank, ICICI Bank, Central Bank of India, and many more. Provide; All you have to do is follow the steps below:

- To download the form go to mudra.org.in or go to the nearest commercial or private bank.

- Submit the loan application form with correct details like your name, address, contact number, and Aadhaar details.

- Submit other documents like identity proof, address proof, company address proof, balance sheet, IT return, and other machinery details along with the application form.

- Performing other formalities and procedures by the bank.

- The verification of the documents will be done by the bank.

- Once verified, the loan will be credited to the applicant’s account.

9. Orient Mahila Vikas Yojana Scheme For Women Entrepreneur

✔ This scheme is provided by Oriental Bank of Commerce to those women who hold a 51% share capital individually or jointly in a proprietary concern.

✔ No collateral security is required for Business loans of ₹10 lakhs up to ₹25 lakhs in case of small-scale industries and the period of repayment is 7 years.

✔ A concession on the interest rate of up to 2% is given.

# Best Small Business Loans in India to go for

Are you looking for a small or a startup business loan? If so, you’ll be happy to read this!

Getting capital loans to start or grow your business may look daunting when you have no proper information. Worry not! These 5 startup business loans by the Govt of India that you can avail to finance your small business.

Small Business Loans in < 1 Hour

Many small businesses are now opting for the ‘MSME Startup Business Loans in 59 Minutes’, a scheme first announced in 2018 by Vyapar with very low business loan interest. The loan is given to small businesses to encourage them to grow their enterprise. This loan is given to businessmen who are yet to start his business. You can avail up to 1 crore. Your loan will be approved within 59 minutes and you will receive the money within 11 days. Interest rate is different for different business and also depends on your credit score.

To apply for small business loans, you just need:

1. GST verification

2. Income Tax verification

3. Bank Account Statements for the last 6 months

4. Business Ownership related documentation

5. KYC details

Prime Minister’s Employment Generations Programme (PMEGP)

Who are eligible?

✔ 18 years old and above.

✔ Must have passed 8th Std to work on the project above Rs 5 lakh in the service sector and above Rs 10 lakh in the manufacturing sector.

✔ Institutions registered under Societies Registration Act- 1860.

✔ Production-based co-operative societies.

✔ Self-help groups and charitable trusts.

Benefits you get from this scheme: Loan Amount and Capital Subsidy –

✔ For General Category: The eligible subsidy is 25% of the cost of the project in rural areas and 15% in urban areas.

✔ For Special Category (including SC/ST/OBC /Minorities/ Women, Ex-Servicemen, Physically handicapped, NER, Hill, and Border areas, etc): The eligible subsidy is 35% of the cost of the project in rural areas and 25% in urban areas.

✔ For the manufacturing sector, the loan limit is Rs 25 lakh and in the business/service sector, it is Rs 10 lakh.

✔ The normal interest rate is applicable to the enterprise from time to time.

✔ The Repayment Schedule ranges from 3 -7 years.

How to register and apply for a loan under PMEGP

✔ To apply for this subsidy, you must submit your application online at kviconline.gov.in.

✔ Then, take the printout of the application and submit it to the respective offices along with a detailed business report and other required documents

NOTE:

✔ 2 weeks training period is mandatory for all the applicants under PMEGP

✔ No collateral security nor any third party guarantee is insisted here.

✔ Any assets created from the bank loan should be collateral to Bank.

Better Solution: Easy Digital Business Loans from Vyapar

Although there are a lot of schemes for a small business loan, there is still much that needs to be done to avail these loans. If you don’t meet the eligibility, it might take up to 12 months to get your loan approved by these GOVT loans.

On the other hand, Accounting Software like Vyapar helps you get guaranteed low business loan interest within 72 hours. Simply apply for a business loan, get a same- day approval, accept the quote and upload your documents digitally for verification. The entire process hardly takes 10-minutes of your time and the verification is completed within 3 working days by Lendingkart.

# 5 Must-Have Financial Documents To Get A Business Loan Easily

Applying for a business loan?

Looking to grow your business but do not have the savings to get up and running. This is where business loans come in. But like most good things, business loans don’t come easily.

Getting a small-business loan isn’t a piece of cake! Especially for small businesses, the lending standards of banks are really tight. Well, although getting approved for business loans is difficult, the more prepared you are, the better.

Having the right business documents in hand increases your chances of getting the loan by 50%!

This is because your loan eligibility is calculated based on your ability to pay it back. Each bank has specific requirements, criteria and eligibility factors to decide if you’re eligible enough.

However, the loan process becomes seamless if your financials, accounting and tax records are up-to-date, accurate and remain organized. i.e Getting a business loan from a bank becomes easier when you have proper financial documents of your business.

Here’s what documents prepare you to get a business loan sooner:

✔ Every moneylender/bank will verify your financial status before approving the business loan.

✔ They expect you to submit your business transaction records preferably audited or reviewed.

✔ It is for this reason, it is advised to maintain account-by-account information with sales details and payment history.

However, a lot of business owners ignore maintaining books as they get too busy with other tasks. Good accounting software for MSME will help the business owner to access any information about business sales/payments/customers with accuracy without manual effort.

✔ The bank will also look at the summary of your outstanding receivables and payables as it is an absolutely necessity.

✔ It gives your bank/lenders a better insight into your business’s financial status and shows your ability to repay a loan.

✔ A healthy cash flow report puts your business at a lower risk of fraud. It is for this reason, transparency into the financial state of your business is an absolute must!

Make sure you have gathered Cash flow statement before applying for a loan. Again, good accounting software like Vyapar App helps you generate cashflow reports without doing any manual background work.

✔ A Profit &Loss statement shows how your profits have been over a period of time.

✔ Your bank might need this to examine your business’s net income or earnings.

✔ If you’reconsistently profitable, then you’re more likely to be considered financially well prepared and equipped to repay the loan taken. Hence, you may have to supply as much profit and loss history as you have.

Need to trace your profits and losses? Try Vyapar App to maintain your business accounts, get to know profits for the day/month/year effortlessly.

✔ Your balance sheet allows people outside of your company to quickly understand its financial condition.

✔ Additionally, banks may use it to understand where their loan amount will go and when they can expect to be repaid. It determines the Risk and Returns involved.

✔ When applying for a loan, the bank will review your balance sheet to see how easily you can manage your financial burden in the short-term.

✔ Not just for the bank, this document helps you know your financial standing and lets you make informed decisions. In addition, it improves your business’s operational efficiency, borrowing habits, and overall financial health.

✔ It can also tell you how long it takes to sell inventory and the length of your accounts receivable. This can help you identify customer buying trends and see how your company’s finances and operations compare to competitors.

✔ Last but not least, the bank will ask to see your business tax returns from the previous year. This is to cross-verify tax return details with the information you’ve supplied through your other financial documents.

Banks will always want these financial documents to judge whether you have the ability to repay the loan or not. Together, these 5 business-financial documents give lenders a perfect picture of your business’s financial health and see if you’re trustworthy to receive the loan.

If you have not been keeping these records right, it is time to start since they could be of help in the future when applying for a loan.

Hence it is very important to use accounting software for all your bookkeeping needs from day 1 of your business.

# 8 Important Things To Do Before Applying For A Business Loan

Not every small business owner has enough money to meet all their needs. Many of them have little option but to borrow money to meet and grow business to the extent they want to.

Back then, taking a loan was a way to misery, something that you did when you could not manage your business finances yourself. However, times have changed and we have reached a situation where taking loans has become the norm of business growth.

Taking small business loans and paying EMI is an absolutely normal activity. Even though it’s the norm, not everyone should opt for a business loan. Also, not everyone is eligible for a business loan.

Here are 8 Important Things You Should Consider Before Applying For A Business Loan.

1. Understand the purpose of taking a business loan.

✔ The first step is to understand why you need the money! See if this will benefit your business for years to come.

✔ Find out for what purposes can the loan amount be used. If not for yourself, the Bank will surely ask you for this.

✔ Many need loans for the purpose of buying more inventory, renting better and bigger space for business, investing in marketing your business, hiring more staff, etc.

✔ Knowing the need for the loan is sometimes vital: If the loan is required to buy business tools and machines, there are a number of banks and NBFCs that provide equipment and machinery loan and equipment finance.

2. Know what the business loan costs you before applying for one.

✔ Taking out a business loan is a big commitment!

✔ Calculate the cost of your business loan. What is the interest rate it attracts, what will be the EMI, for how many years are you prepared to take the burden and so on.

✔ A business loan does have a huge price attached. Make sure you’re aware of the consequences.

3. Work out the business loan amount you’re planning to borrow.

✔ Find out how much money you are falling short off in growing your business. You may have to apply for a business loan accordingly.

✔ You may be eligible for a higher amount, but it is not necessary to borrow that amount. By borrowing too much, you’ll struggle to repay the loan. Borrowing too little, you may end up applying for secondary loans too.

✔ However, it can be a challenge to figure out how much to borrow. Calculations go wrong, you may underestimate or overestimate the cost of a few and very few things go exactly as planned. Always take a little higher than needed just in case of unexpected expenses. Not more, not less.

✔ Also, try to arrange the maximum of the down payment amount and less of the business loan amount so that the interest is kept at minimal. Never take too much risk.

4. Calculate your capacity for collateral.

✔ In simple words, you will be instantly eligible for loans if you have sufficient collateral. At least, your loan application won’t immediately be rejected if you have sufficient collateral.

✔ Banks feel much more comfortable if you have assets that can repay loans in the worst case.

✔ Collateral includes your houses, cars, stocks, bonds, and cash –– all things that are readily convertible into cash to repay the loan.

✔ But, for small business loans, the banks consider even your assets such as equipment, accounts receivable, and (in some cases) inventory as collateral if they can be sold by the bank for cash.

5. Research all the borrowing options to find the right fit.

✔ There are a lot of ways to secure loans. Some borrow from family or friends, others use credit cards. Still, others seek business loans from small finance companies, online lenders for a faster loan process without collateral requirements. Often, banks are the first place people look.

✔ Look specifically for “small businesses loans”, this increases your chance of getting the capital you need. Fully understand the terms of your loan, including the total cost of capital and the payment schedule.

6. Understand the interests and charges it carries.

✔ Different banks have different loan schemes.

✔ Shortlist a few banks or NBFCs that you may want to apply for loans. Check what is offered to you in terms of a loan.

✔ While we often only look at interest rates, there are many other aspects to consider before we decide which offer to take.

✔ See what suits you the best and what may work out for you based on how much EMI you can afford.

7. Prepare your financial documents well.

✔ Have your business finances in order. Especially for no-collateral loans, banks are very particular about whom they extend the money.

✔ Keeping proper books of accounts is very important before applying for a loan. It is vital that you go through them to clean out errors.

✔ Banks generally ask for the balance sheet of the company, profit and loss accounts, cash flow statements, tax audit reports, etc.

✔ Beyond these financial statements, you may be asked to provide current year business performance and it is important to get this right. The bank has to make sure that you’re able to repay the loan on time.

✔ If you’re digitally managing your business accounts using billing software like Vyapar App, you are saved! It eliminates lots of unnecessary time & effort involved to get this done.

8. Calculate what you can afford to repay and how to go about the rest.

✔ Take a loan that you can easily repay. Never ever borrow more than you can repay.

✔ Calculate your loan to income ratio. This is what bank calculates too – ‘how much you can afford to repay’.

✔ The loan you can borrow depends on how much you can afford to repay in EMIs.

# 5 Reasons For Your Business Loan To Be Rejected: What You Can Do About It

Every bank checks how reliable you’re when it comes to paying back. Low CS or no collateral says you’re not trustworthy.

The FIX: There are more options out there for you than ever before. Try banks that have no such constraints

If you’re not consistently making profits, that can be a red flag. This says that you’re not managing your business well.

The FIX: Use accounting software that gives you business reports; then, monitor your cash flow weekly & make informed decisions to stay on top of it.

78% of business owners maintain accounts on papers that are lost with time. Sadly, most banks ask for organized financial statements of the business.

The FIX: Start using accounting software to manage your accounts digitally. This way, accessing any business-related details becomes super easy.

When your past performance records say nothing, then getting a loan becomes hard. Build credibility, before applying for a loan.

The FIX: If you are a first-time business owner, try alternative funding channels such as family & friends, credit cards, and small business loans by the government.

The bank needs to know where you will invest money on. If you have no strong purpose, they are less likely to process your loan.

The FIX: Why do you need a loan? Is it for purchasing essential equipment, inventory, or renovating your store? Give a strong purpose for getting a loan.

Frequently Asked Questions(FAQs’)

# What is a Business Loan?

Business loan is an unsecured loan of 1-3 years by banks, NBFCs (Non-Banking Finance Companies) or P2P lending platforms without any collateral, guarantor or hypothecation of any asset. Entities like proprietorship, partnership, private limited company or public limited company are eligible for this type of loan. Business loans are left at the discretion of the borrower and can be used for working capital purposes, meeting short-term cash flow requirements, investment in plant and machinery, etc.

# Should I Get a Business Loan?

It depends on your expectations of the company. Business loans do not give the lender equity in your company. If you are successful you will only have to pay the principal and interest, not a portion of the profits as long as the company exists. A loan also reduces administrative paperwork and duties, such as holding shareholder meetings and votes, and complying with Securities and Exchange Commission rules on investments.

# What do I need to apply for a business loan?

The lending requirements depend on who you are seeking the loan from. For a commercial lender, you need a business plan that outlines a path to profitability, at least enough to service the loan. Unless you have operated a business for several years, you will rely on your personal credentials, such as a good credit score, collateral and experience in your field, to get a loan.

# What do I need money for?

If you determine that it is time for you to take out a loan, the next business loan question you should ask yourself is what you need the money for. You may need loan amount:

- Start your business

- Purchase new equipment

- Stock up on inventory

- Hire employees

- Market your company

- Improve cash flow

- Expand your business

- Help recover from Covid-19 (e.g., PPP loan)

Briefly describe what you need the money for. This can help you determine what type of loan is best suited for your business. Maybe you are just starting your entrepreneurial journey. If that’s the case, an SBA microloan may be a good place to start.

# Can I get a business loan without collateral?

Yes, you can get a business loan without any collateral or security.

# I am looking for an SME loan. Is Business Loan Ideal for SMEs?

Yes, SMEs can avail our Business Loan to purchase equipment, property & even meet the working capital needs of the organization.

# Can Mudra Loan Application Form be submitted online?

Yes, you can apply online by visiting the official website Mudra Loan – www.mudra.org.in, but to apply for a business loan, you must have a proper business plan.

# What is a Mudra card?

It is a digital facility launched by the National Partnership for Community Leadership(NPCL) for working capital needs under the cash loan of Mudra loan provided by RuPay branding.

# Is the Mudra loan offered by all banks in India?

Yes, Mudra loans are offered by almost every private and public sector bank in India.

# What is the processing time of the MUDRA loan?

In general, in the case of the Mudra loan scheme under PMMY, it takes about 7-10 working days for loan approval by banks.

# How can I check my Mudra Loan Status?

You can check your Mudra loan status online through the website of the concerned bank and its e-Mudra loan application status section.

Stay updated about the Latest News on Vyaparapp

Download the BEST GST Compliant Mobile Billing App

Happy Vyaparing!!!