Trusted by 10+ Million Businesses

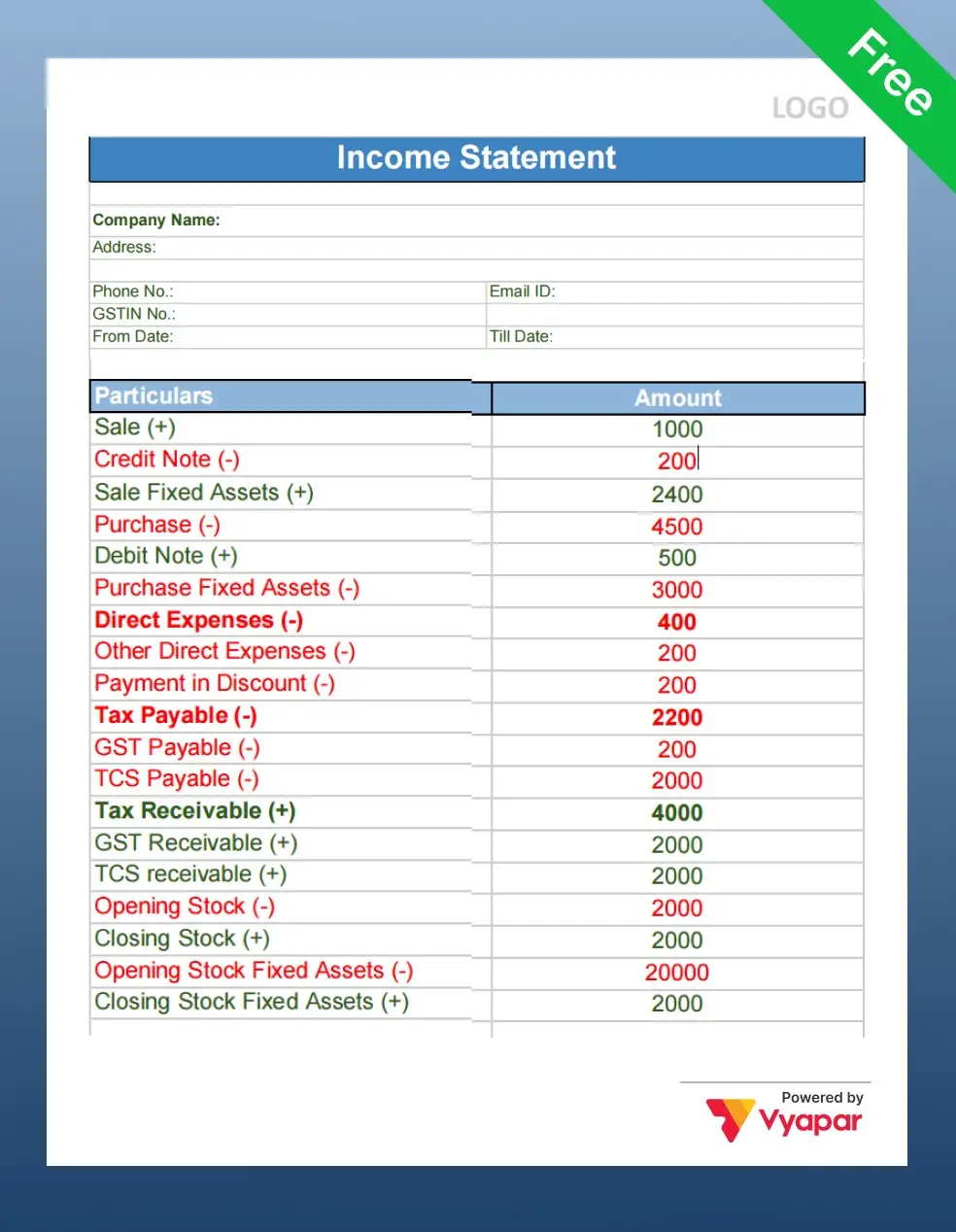

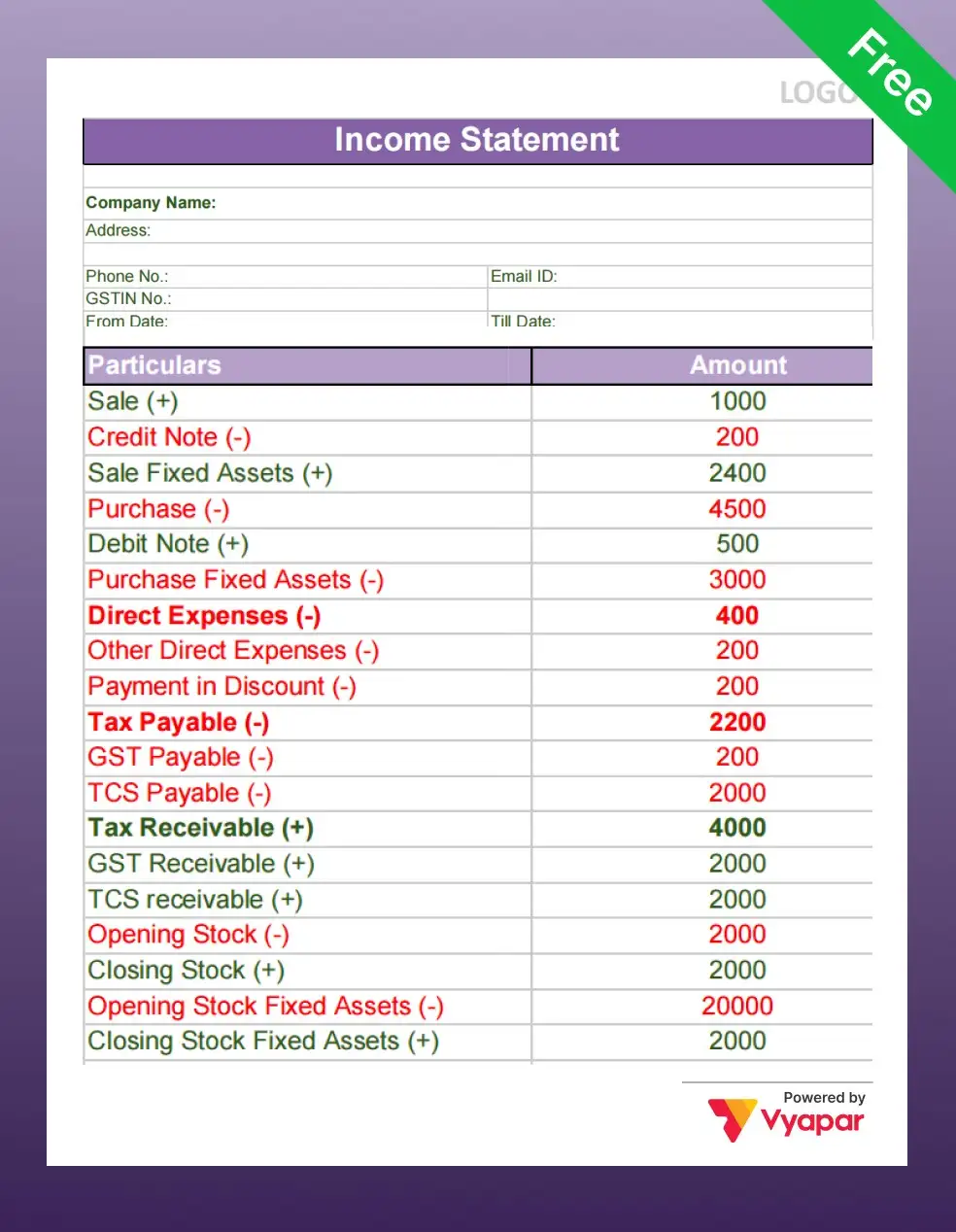

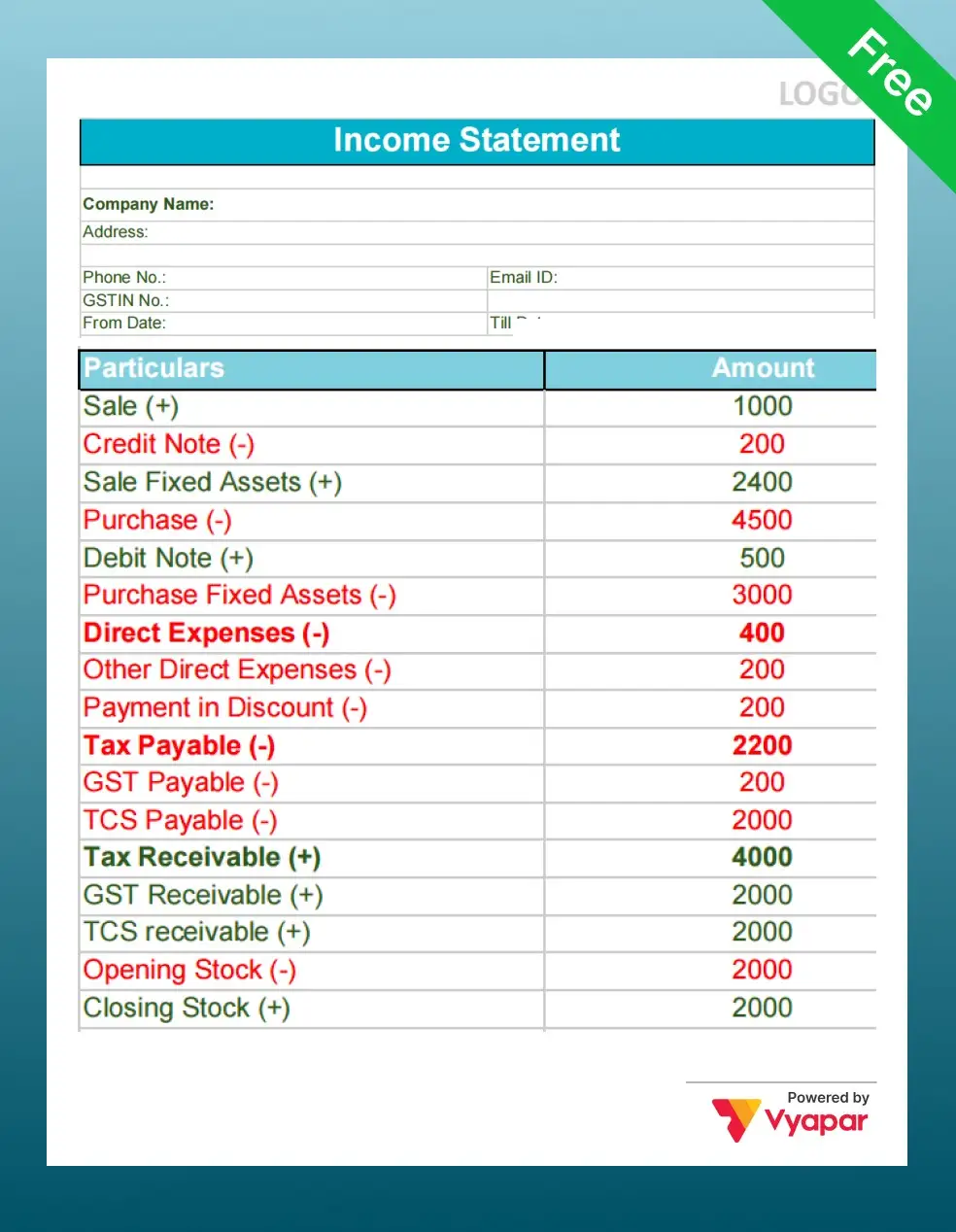

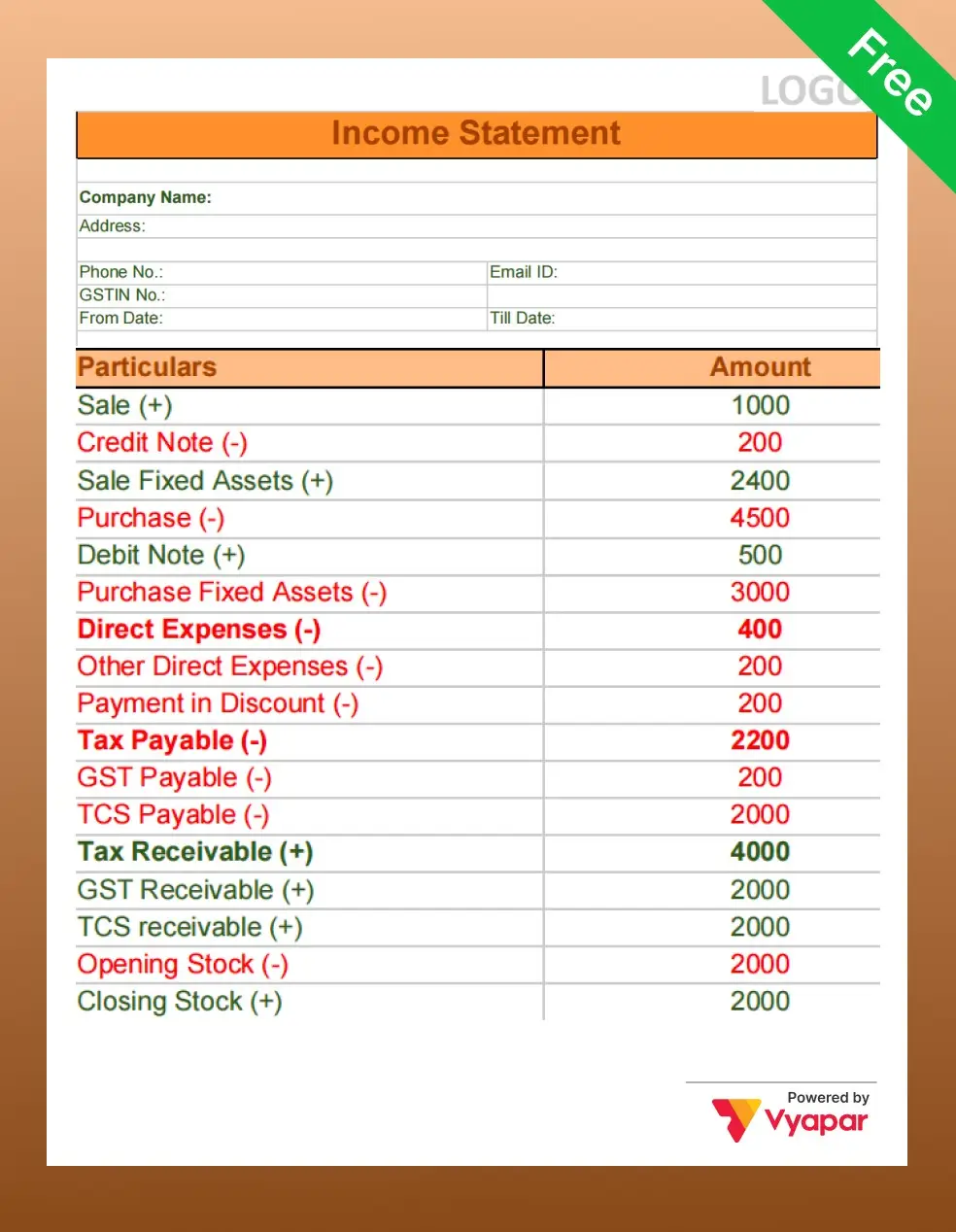

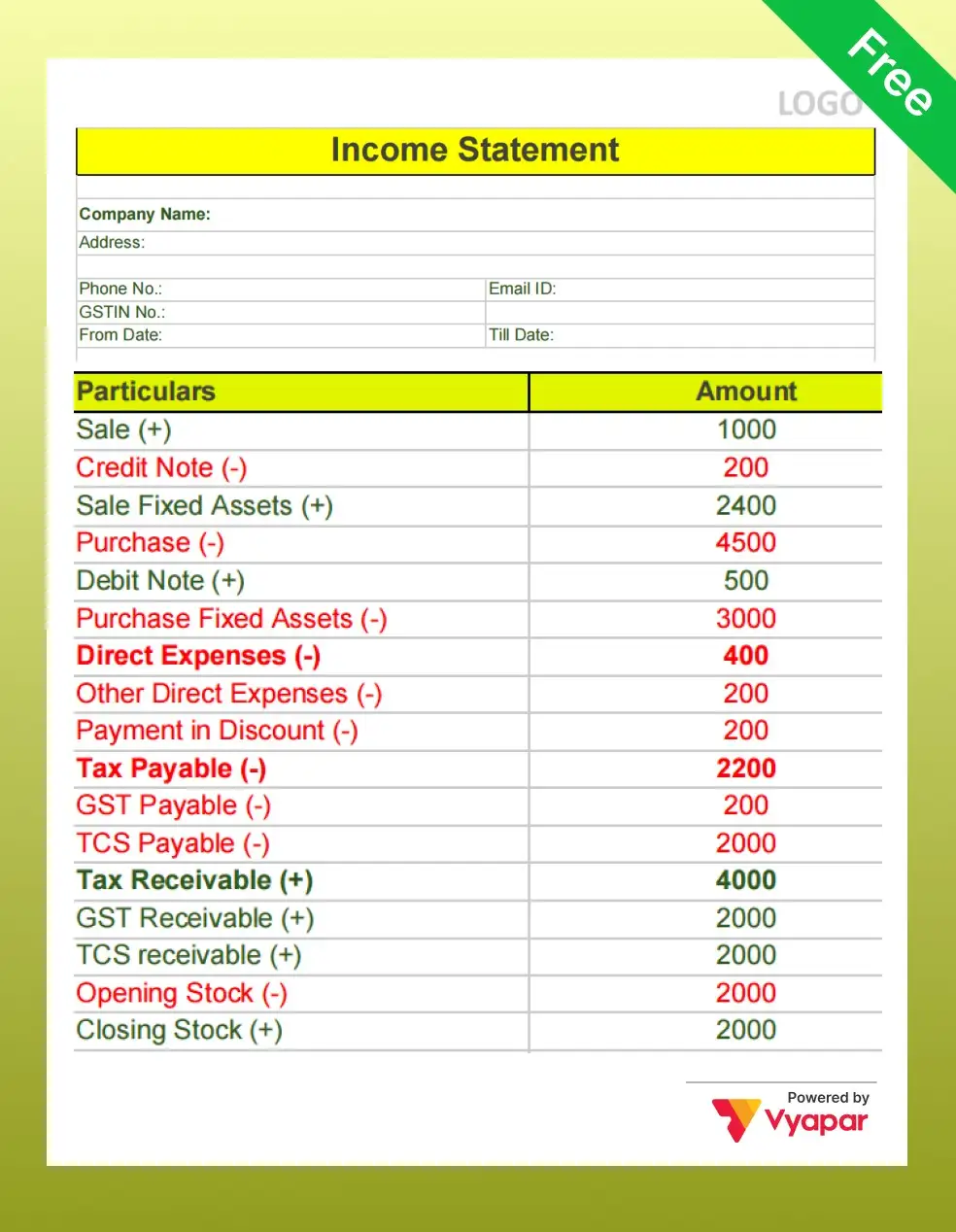

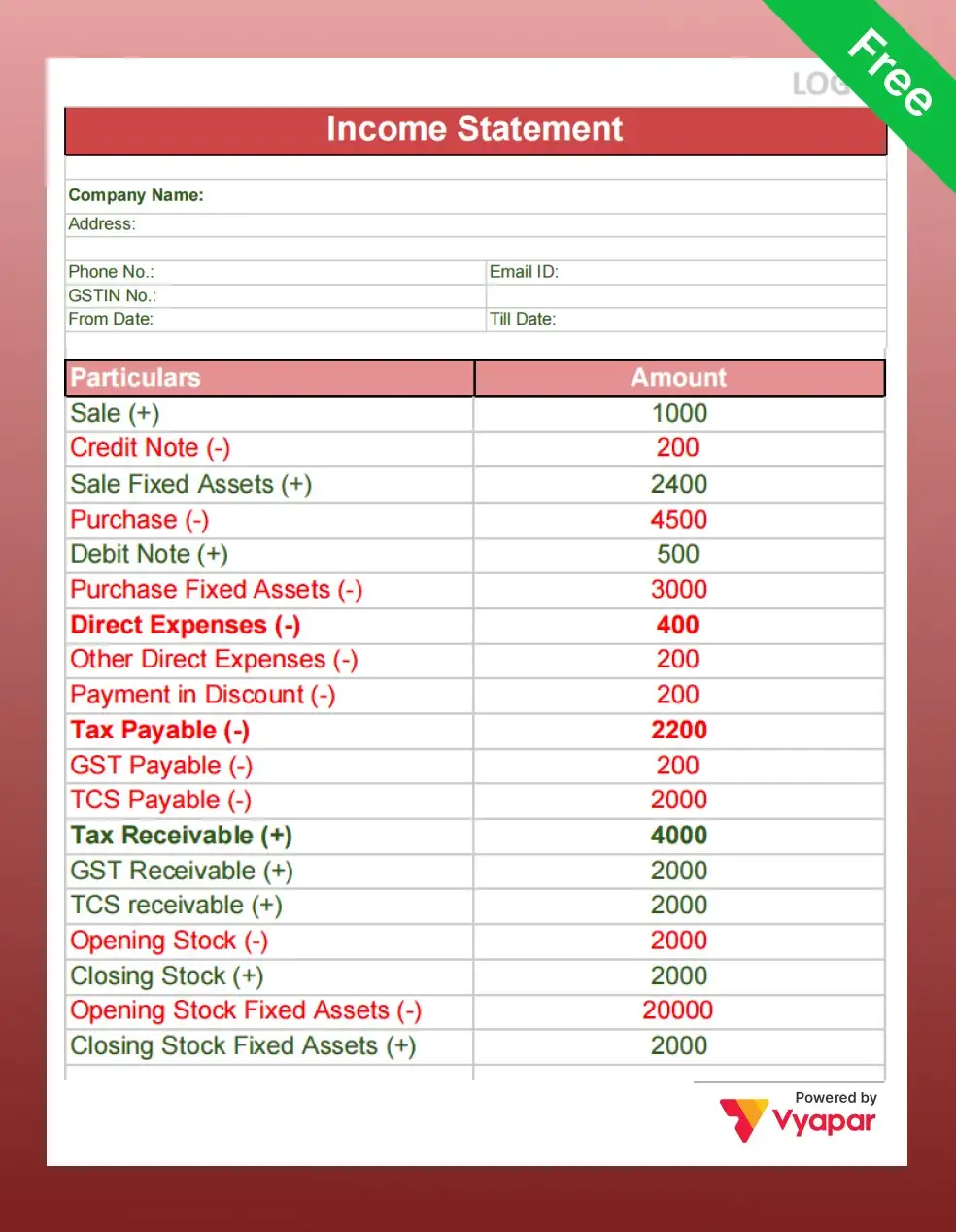

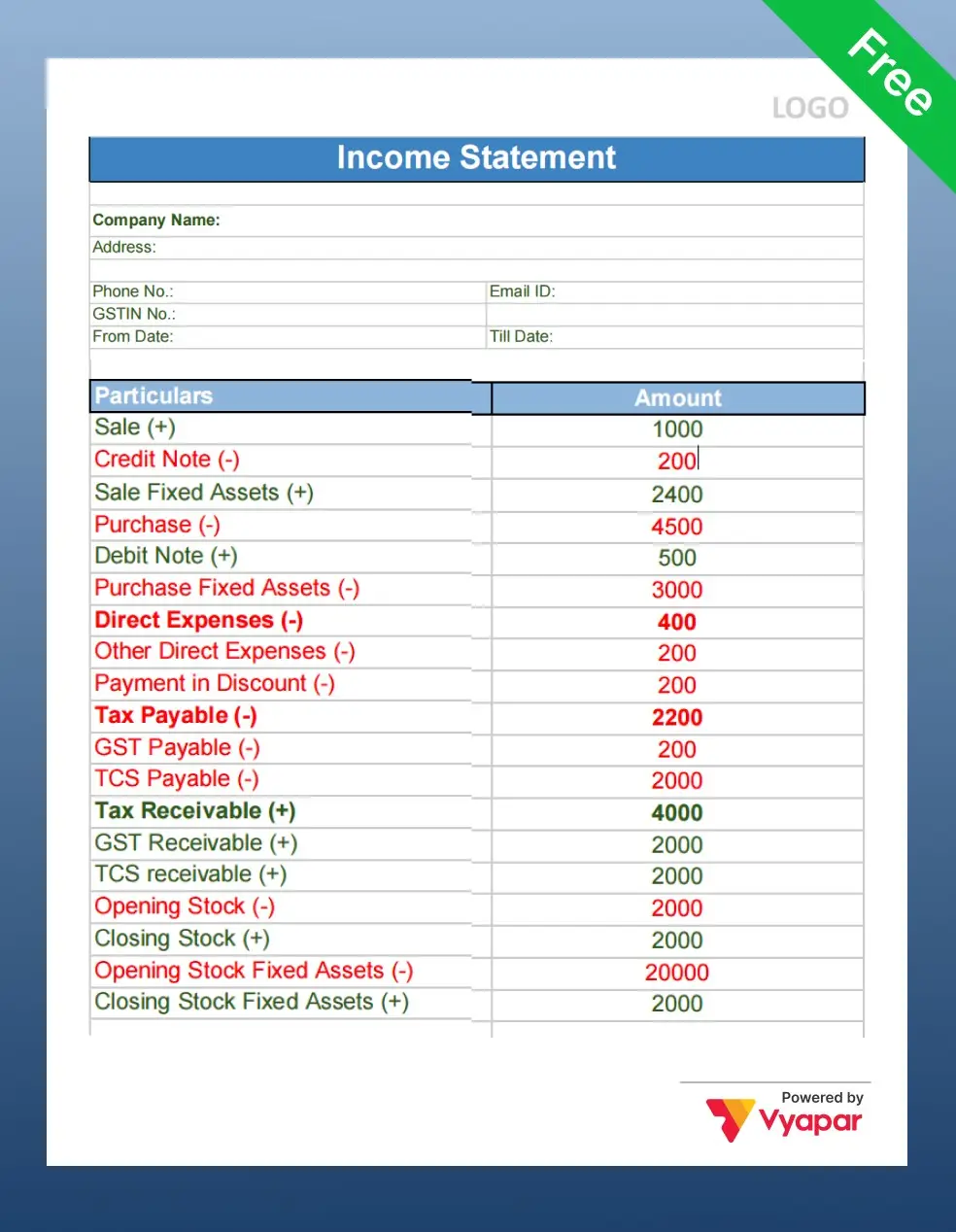

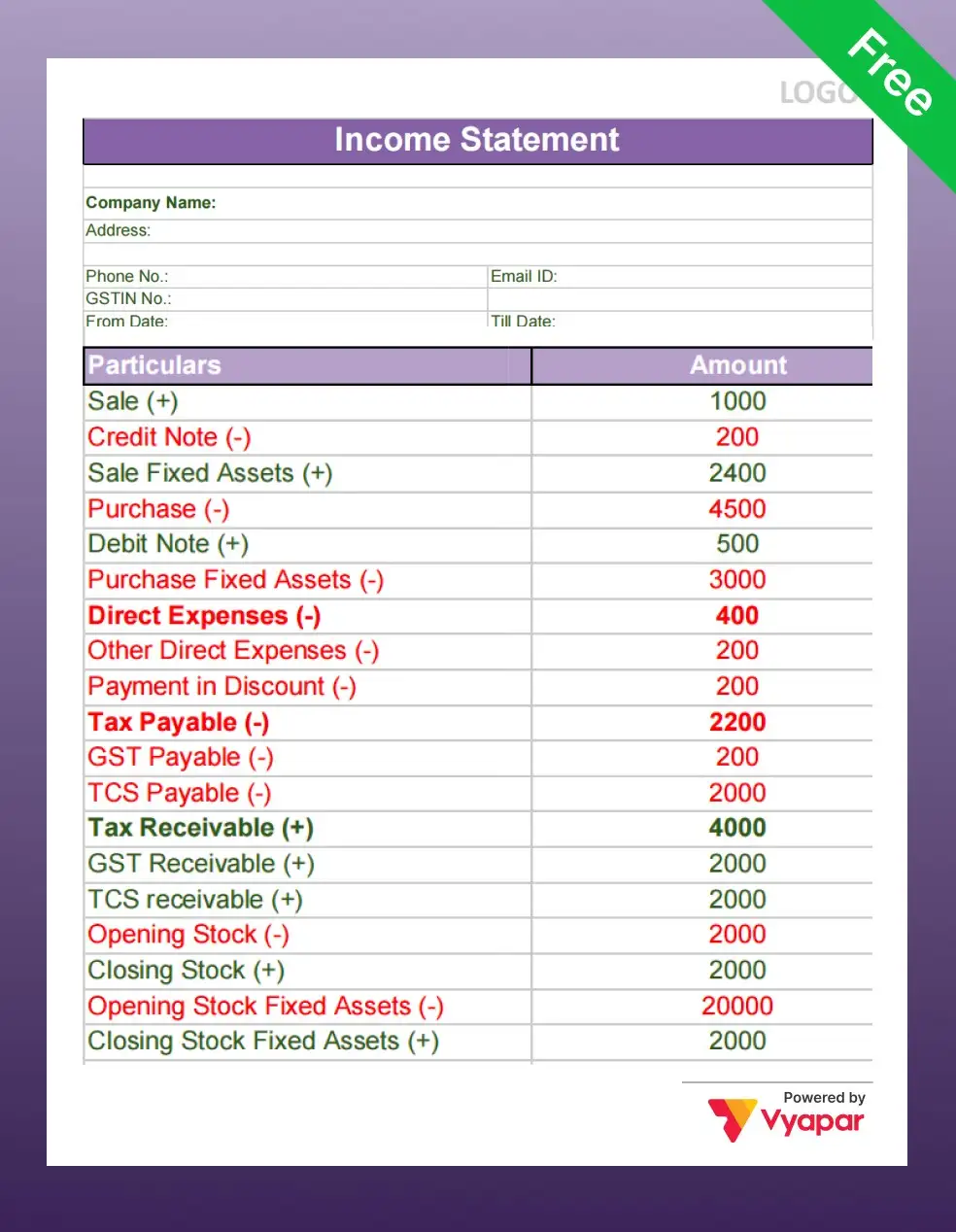

Income Statement Format

Download Professional Templates

Download ready-to-use income statement format templates in Excel, PDF, and Word for free. Track your revenue, expenses, and net profit for any period.

Free Downloads

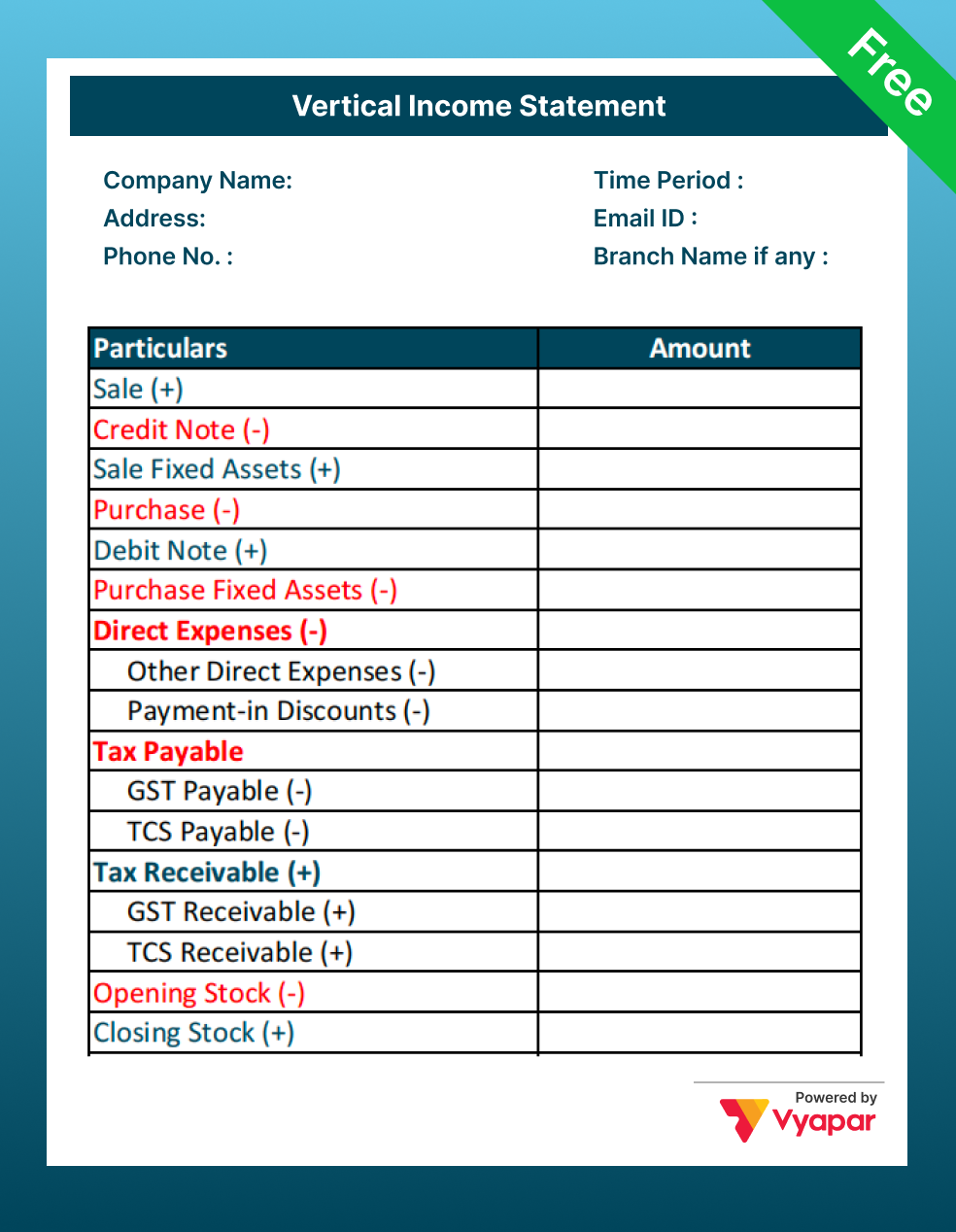

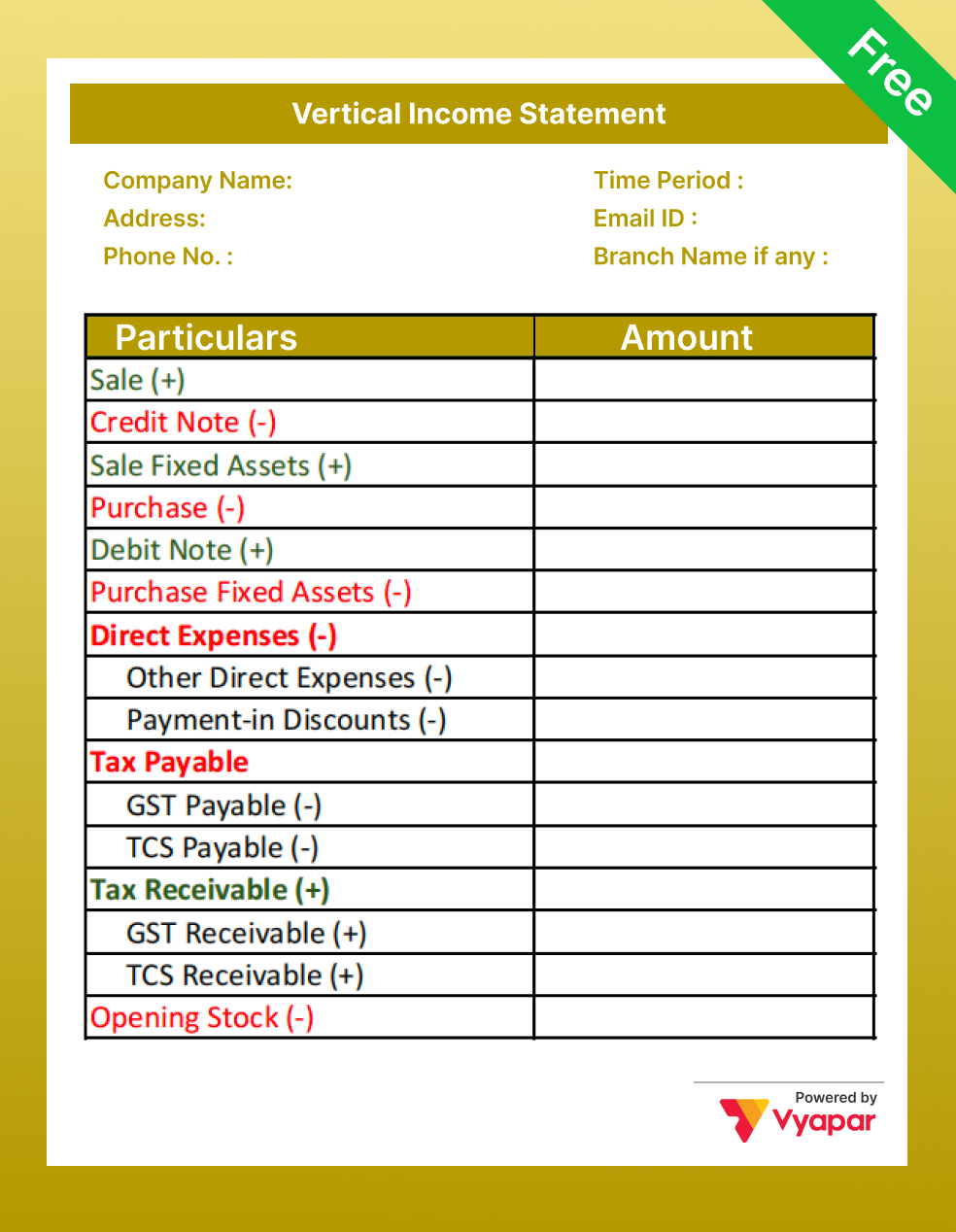

Income Statement Templates

Ready-to-use formats. Filter by file type – Word, Excel and PDF.

Filter by Format

Word

Excel

Filter by Types

P&L Statement

Vertical Analysis

Multi-Step

Annual Income

No templates found

Try adjusting your filters to find the templates you’re looking for.

Quick Guide

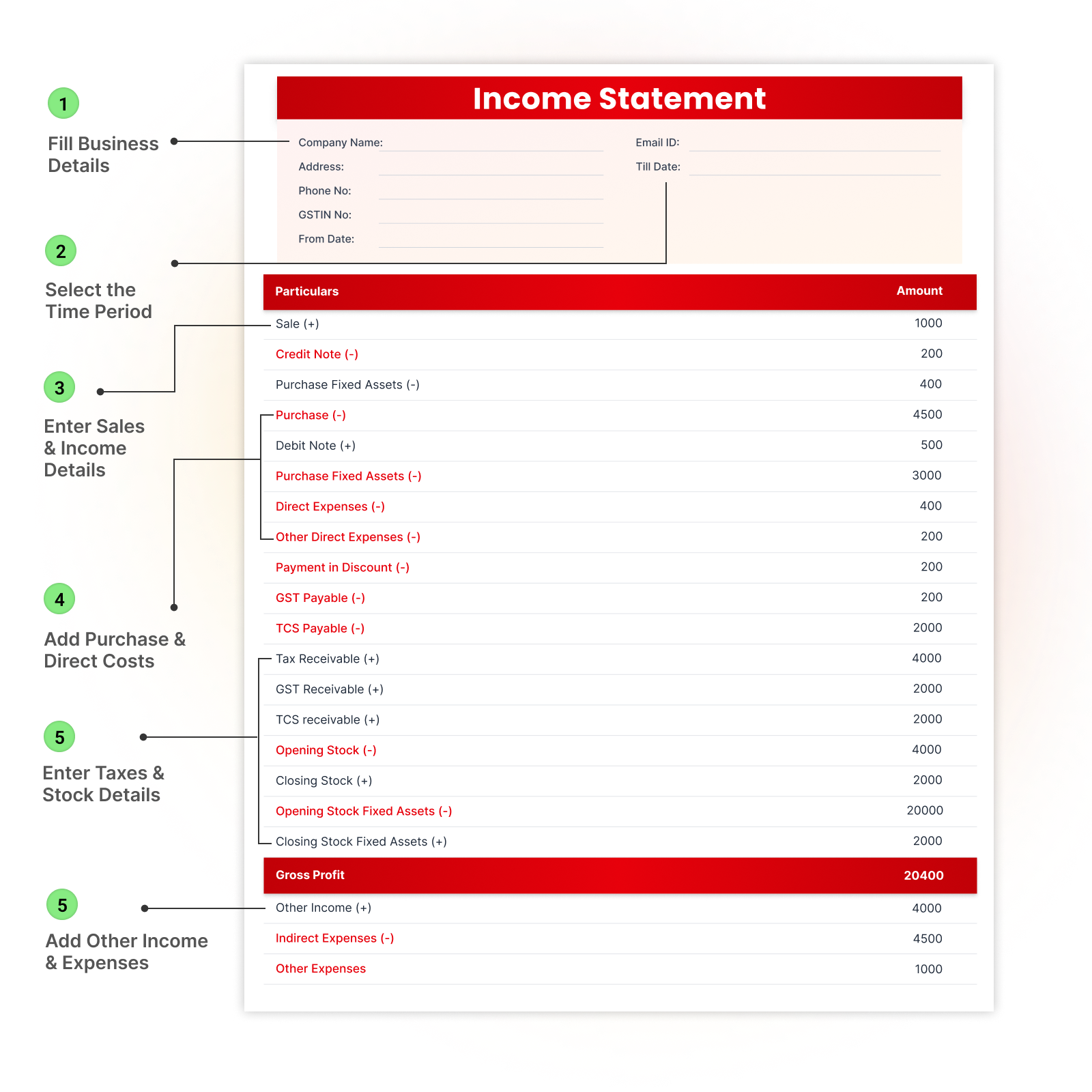

How to Use an Income Statement

01

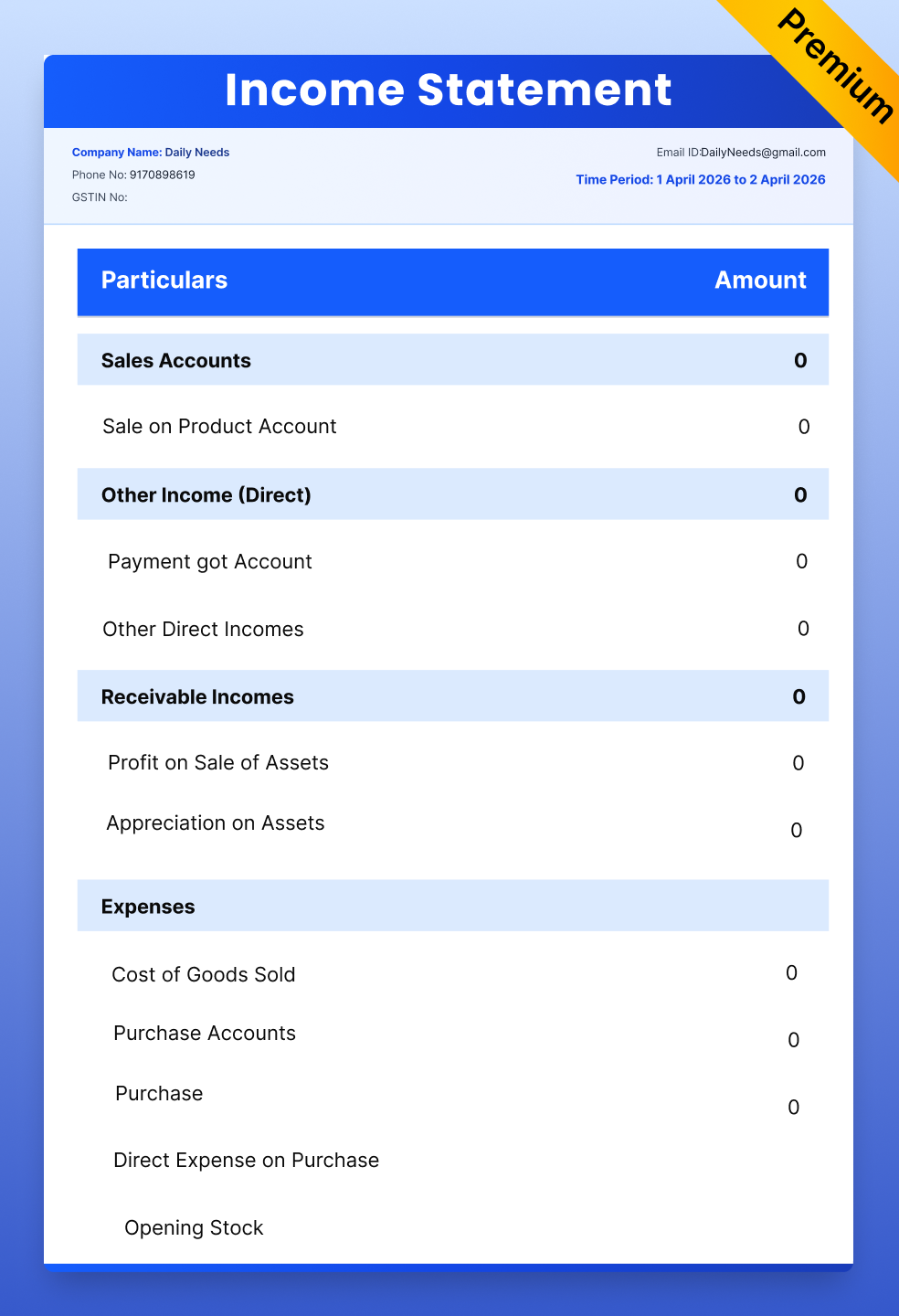

Fill Business Details

Enter the company name, address, contact details, and GSTIN to identify your business.

02

Select Time Period

Add From Date and Till Date to define the reporting period.

03

Enter Sales & Income

Fill sales, subtract credit notes, and add any other income.

04

Add Purchases & Costs

Enter purchases, returns, and all direct expenses.

05

Enter Taxes & Stock

Fill tax details and opening/closing stock to adjust profit.

06

Add Other Expenses

Include indirect expenses and charges to get the final profit.

Formats Explained

Types of Income Statement Format

Not all income statements follow the same layout. Depending on your business type and reporting need, you can use one of two formats:

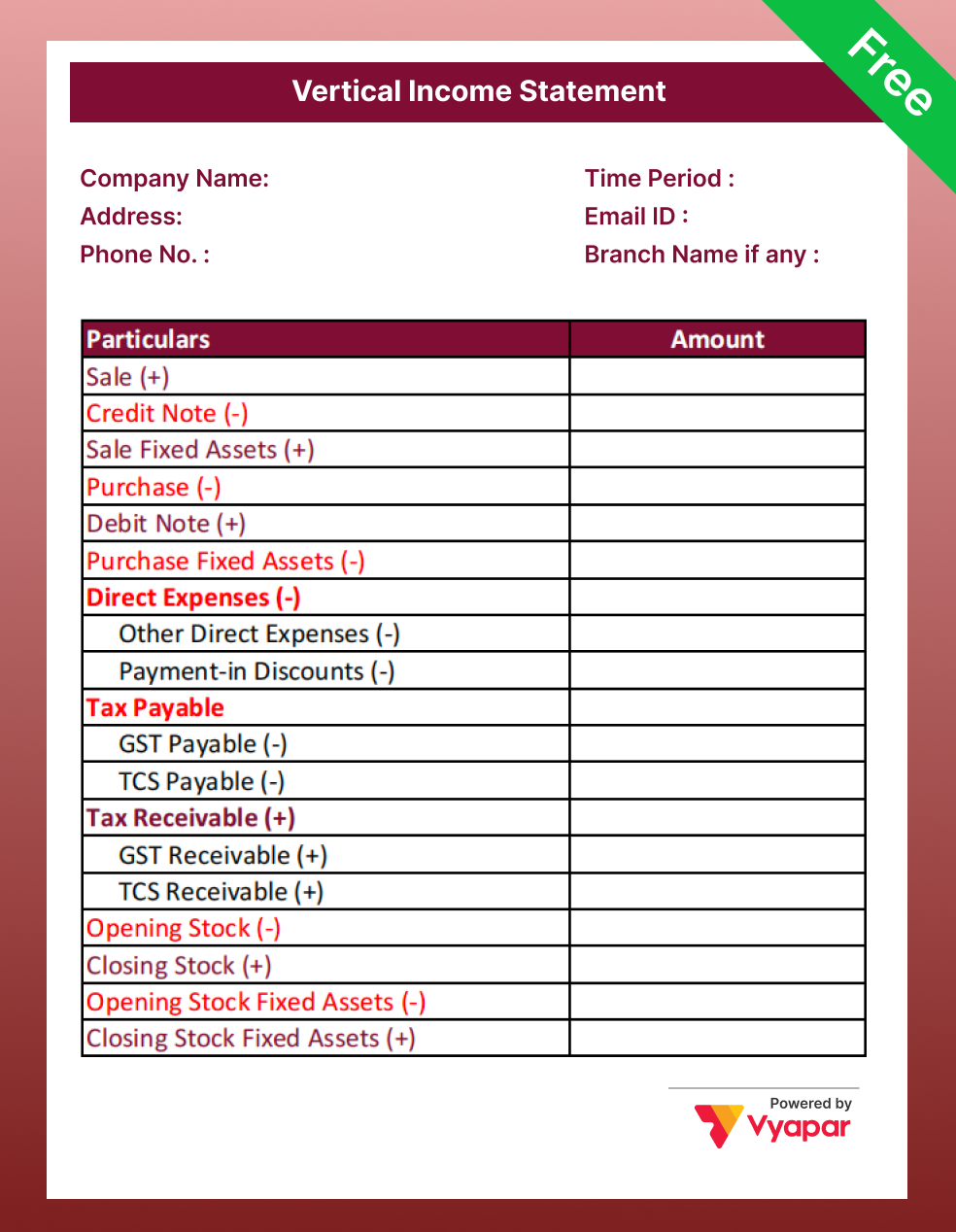

Single-Step Income Statement Format

The single-step format is the simplest approach. It groups all revenue together at the top and all expenses below, then subtracts one from the other to arrive at net profit or loss. There are no subtotals like gross profit or operating profit – just one calculation at the end.

This format works best for freelancers, consultants, and small service-based businesses in India that have straightforward income and expenses with no cost of goods sold. It is quick to prepare and easy to read.

Multi-Step Income Statement Format

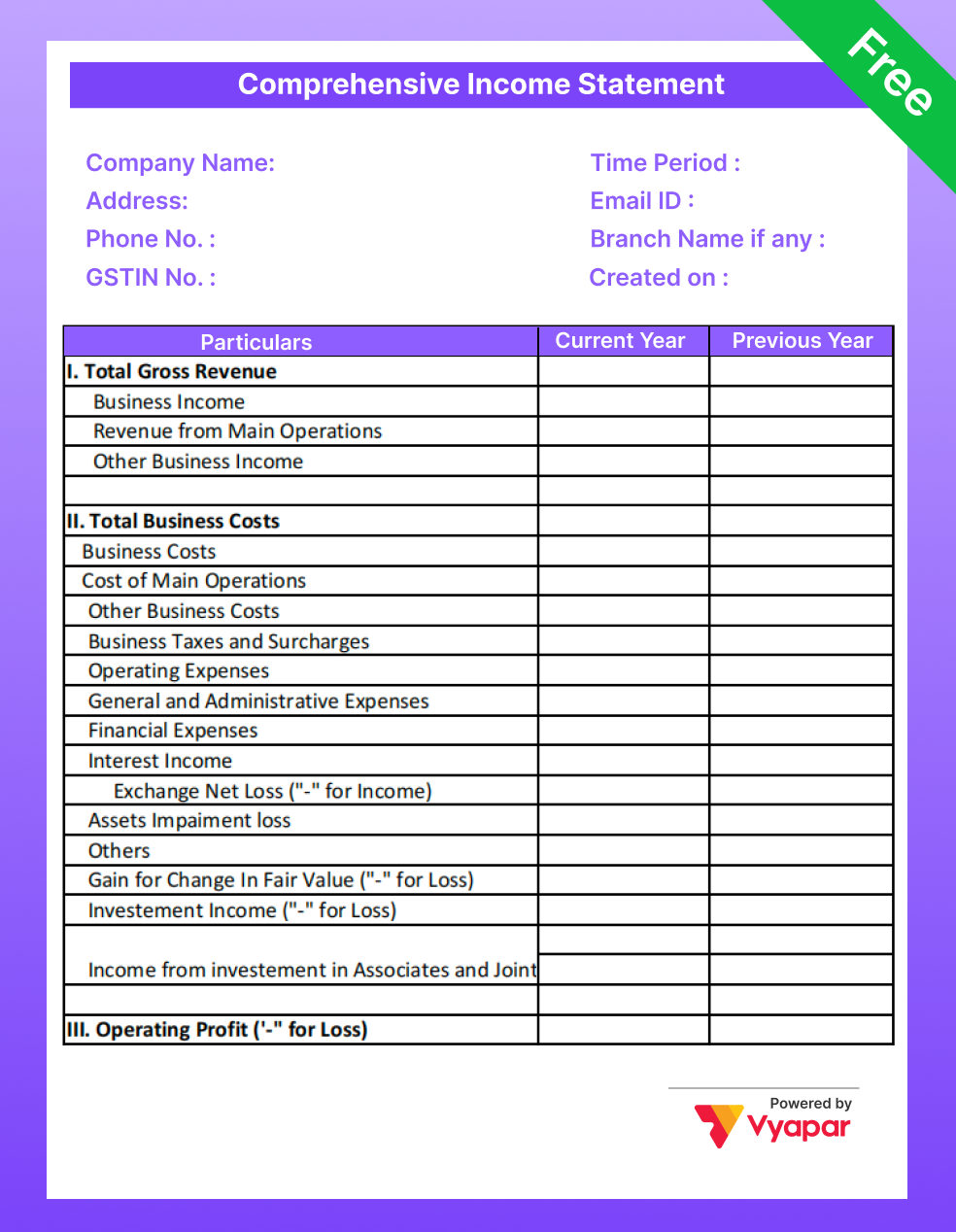

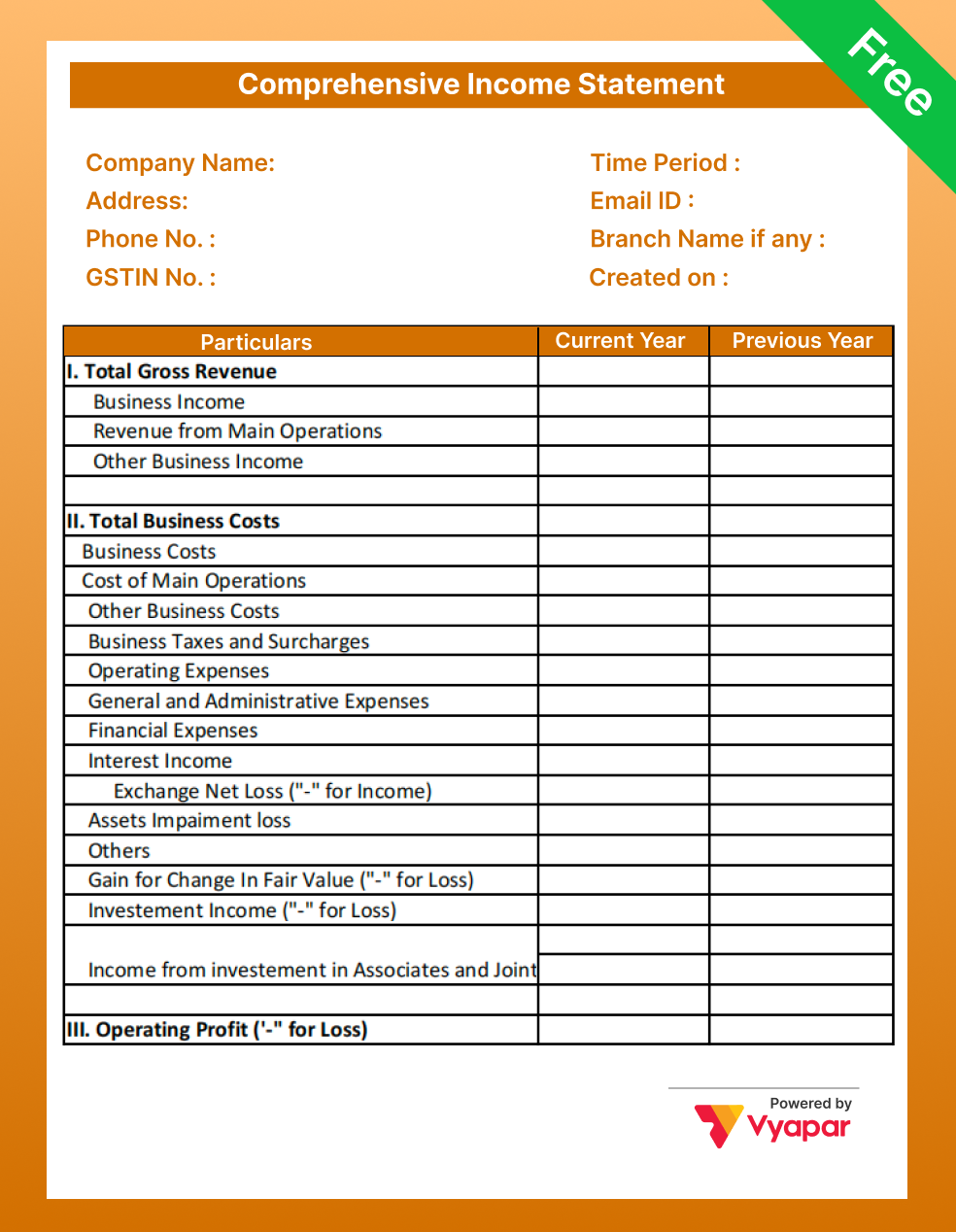

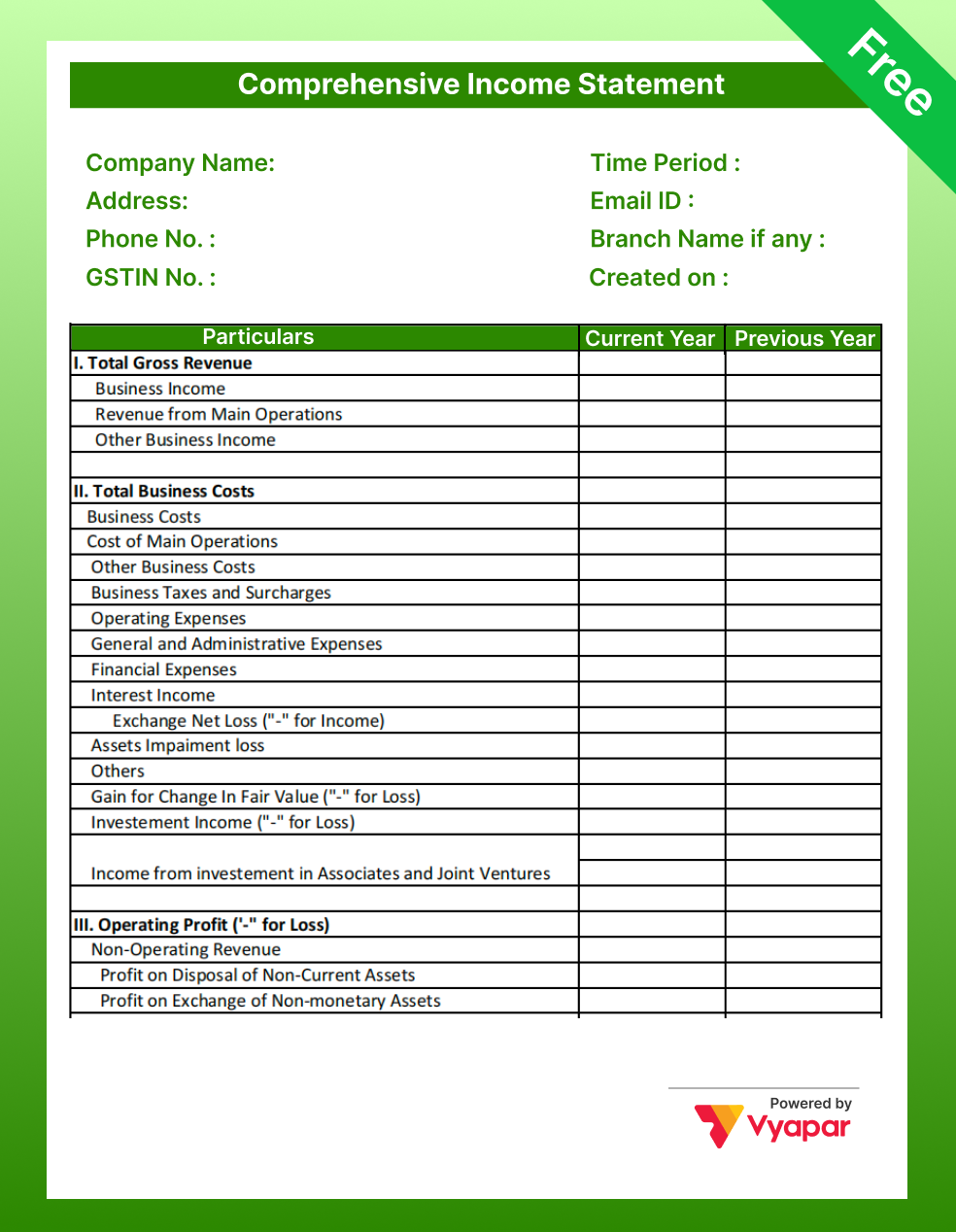

The multi-step format breaks the statement into stages, showing gross profit first, then operating profit, and finally net profit after taxes and interest. Each stage gives you a separate view of how your business is performing at different levels.

This format is better suited for traders, retailers, and manufacturers who need to track cost of goods sold separately from operating expenses. It gives a more detailed picture of where the business is making or losing money. Most Indian small businesses that maintain proper accounts use the multi-step format.

Understanding the Basics

Key Components of an Income Statement Format

Revenue (Sales / Turnover)

Revenue is the total income your business earns from its primary operations during the period. For a retail shop in India, this is the total value of goods sold. For a service business like a CA firm or IT consultant, this is the total fees billed to clients. Under GST, revenue is typically recorded as the taxable value excluding GST collected.

Cost of Goods Sold (COGS)

COGS includes all direct costs involved in producing or purchasing the goods your business sells – raw materials, purchase price of stock, and direct labour. For a service business, this line is usually absent or replaced by direct service delivery costs. Subtracting COGS from revenue gives you gross profit.

Gross Profit

Gross profit shows how much your business earns after covering the direct cost of what it sells, before accounting for overhead expenses. A healthy gross profit margin means your core business activity is profitable. For Indian MSMEs, monitoring gross profit monthly helps identify pricing or procurement issues early.

Operating Expenses

These are the indirect costs of running your business – staff salaries, shop rent, electricity, internet, marketing spend, and GST filing charges. operating expenses not tied to producing a specific product or service but are necessary for day-to-day operations. Subtracting operating expenses from gross profit gives you operating profit.

Net Profit or Loss

Net profit is the final bottom line – what remains after deducting all expenses, interest on loans, and applicable taxes from total revenue. If the result is positive, your business made a profit. If negative, it is a loss. This is the number that banks, investors, and tax authorities look at when evaluating your business.

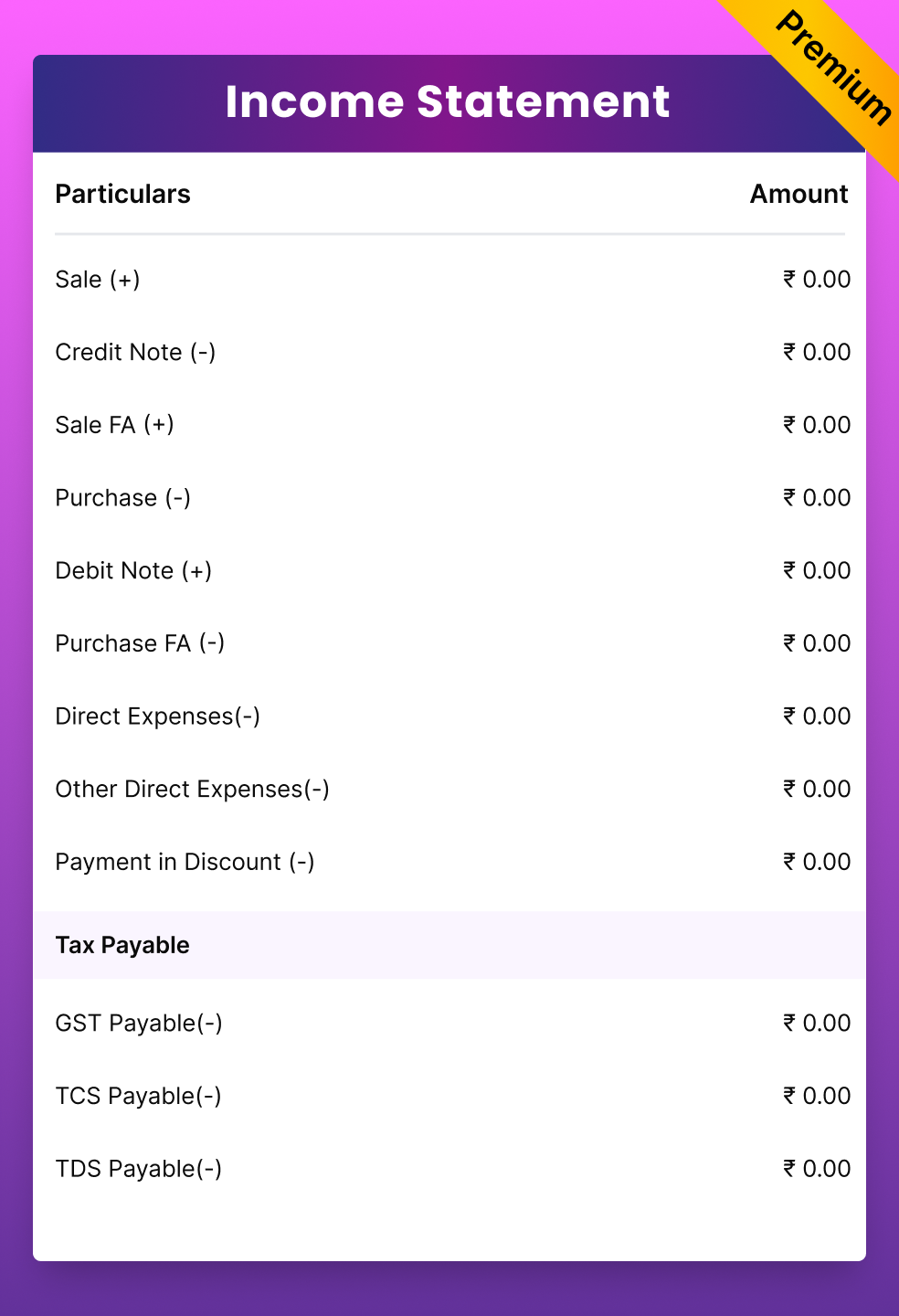

Premium Collection

Premium Income Templates

Access our exclusive premium collection with advanced features

Comprehensive P&L Statement Format

Detailed Income Statement

Go Beyond Templates

Why 1.5 Crore+ Businesses Choose Vyapar

More than just formats – a complete business management solution

Instant Billing

Create bills in seconds

100+ Formats

GST, retail, service & more

Smart Reports

Track sales & profits

Offline Billing

Access without internet

Everything you need to run your business

- Auto GST calculations

- Inventory management

- Payment reminders

- Multi-device sync

Available in Android, iOS, Mac and Windows

Got Questions?

Frequently Asked Questions

Find answers to common questions about income statement formats

What is an income statement format?

An income statement format is a structured financial document that presents a business’s revenues, expenses, and net profit or loss over a specific period – typically a month, quarter, or financial year. It follows a standard layout starting with total revenue at the top, subtracting cost of goods sold (COGS) to arrive at gross profit, then deducting operating expenses to show net profit or loss. In India, it is also commonly called a profit and loss (P&L) statement.

What are the components of an income statement format?

A standard income statement format includes the following components:

- Revenue / Sales – total income earned from business operations

- Cost of Goods Sold (COGS) – direct costs of producing goods or services

- Gross Profit – revenue minus COGS

- Operating Expenses – rent, salaries, utilities, and other indirect costs

- Operating Profit (EBIT) – gross profit minus operating expenses

- Tax and Interest – applicable deductions

- Net Profit or Loss – the final bottom line after all deductions

What is the format of an income statement for small businesses in India?

For small businesses in India, the income statement format typically includes total sales or service income at the top, followed by direct costs, gross profit, and then common operating expenses like staff salaries, rent, and office expenses. The final figure shows net profit or loss for the period. Under GST, businesses may also separate taxable and exempt income within the statement for clarity.

What is the difference between an income statement and a balance sheet?

An income statement shows how much a business earned and spent over a period of time – it measures performance. A balance sheet shows what a business owns and owes at a single point in time – it measures financial position. Both are part of a complete set of financial statements, but they answer different questions. The net profit from the income statement flows into the equity section of the balance sheet.

Is an income statement the same as a profit and loss statement?

Yes, an income statement and a profit and loss (P&L) statement are the same document. In India, the term P&L statement is more commonly used by small business owners and accountants, while the income statement is the standard term used in formal accounting and under IFRS or Ind AS reporting standards.

What is the income statement format in Excel?

An income statement format in Excel typically uses rows for each line item – revenue, COGS, gross profit, expenses, and net profit – with a formula-driven structure so totals calculate automatically. Excel templates allow businesses to update figures monthly and track trends over time. You can download a free income statement format in Excel above, which is pre-formatted and ready to use.

How do I prepare an income statement format for my business?

To prepare an income statement for your business: start with your total revenue for the period, subtract the cost of goods sold to get gross profit, then list and subtract all operating expenses such as rent, salaries, and marketing costs. The result is your operating profit. After accounting for taxes and interest, you arrive at net profit or loss. Using a ready-made income statement template simplifies this process significantly.

What time period does an income statement cover?

An income statement can cover any defined period – monthly, quarterly, or annually. Most small businesses in India prepare a monthly P&L to track performance and an annual income statement for tax filing and compliance purposes. The time period must always be clearly stated at the top of the statement.