List of Accounting Standards in India (AS 1–AS 32)

KEY TAKEAWAYS

- India has 32 Accounting Standards (AS 1–AS 32)

- Core standards like AS 1, AS 2, AS 3, AS 9, and AS 10 are most relevant

- Some standards are merged or withdrawn

- Accounting Standards ensure consistency and compliance

Introduction

Accounting Standards in India define how businesses record, present, and report financial transactions. Issued by the Institute of Chartered Accountants of India (ICAI), these standards ensure consistency, transparency, and accuracy in financial statements.

For small and medium businesses, understanding these standards helps maintain proper books of accounts, comply with tax regulations, and make informed financial decisions.

Meaning of Accounting Standards

“What do you mean by Accounting Standards?”

Accounting Standards are a set of guidelines that govern how financial transactions should be recognized, measured, and disclosed in financial statements.

They help answer critical questions such as:

- When should revenue be recorded?

- How should inventory be valued?

- What financial information must be disclosed?

Using accounting software helps implement these standards consistently in daily operations.

By following these standards, businesses ensure their financial data is reliable and comparable across periods.

Overview of Accounting Standards in India

India has issued 32 Accounting Standards (AS 1 to AS 32) under Generally Accepted Accounting Principles (GAAP). However, not all are currently active, as some have been merged or withdrawn.

For most small businesses, only a few key standards are used regularly in day-to-day accounting.

Key Accounting Standards for Businesses

The following standards are most relevant for billing, inventory, and financial reporting:

Complete List of Accounting Standards

These guidelines ensure consistency for preparers, auditors, and stakeholders when managing financial statements.

Core Standards

Better does not always mean expensive. It means useful, reliable, and designed for your type of business. A good accounting software for small businesses helps you see the full picture.

| Standard | Description |

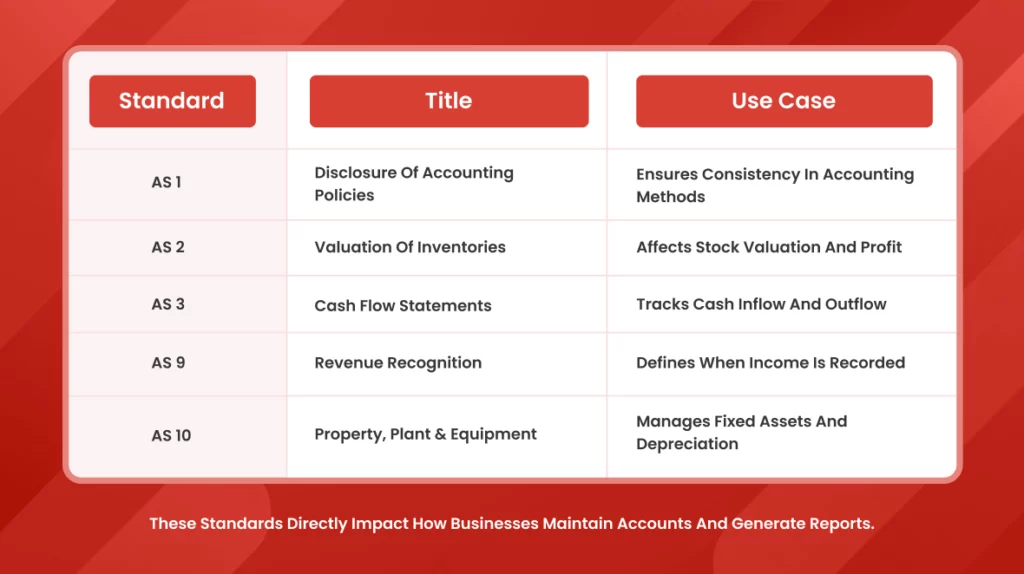

| AS 1 | Defines the disclosure of accounting policies followed by a business to ensure consistency and transparency in financial reporting. |

| AS 2 | Covers valuation of inventory, including raw materials and finished goods, to determine accurate cost and profit. |

| AS 3 | Focuses on cash flow statements, showing inflow and outflow of cash from operating, investing, and financing activities. |

| AS 4 | Deals with contingencies and events occurring after the balance sheet date that may impact financial statements. |

| AS 5 | Specifies treatment of net profit or loss, including prior period items and changes in accounting policies. |

Check Out – How to Check Your Balance Sheet in Vyapar App

Operational Standards

| Standard | Description |

| AS 7 | Applies to construction contracts and defines how revenue and costs should be recognized over the contract period. |

| AS 9 | Establishes rules for revenue recognition, ensuring income is recorded when it is earned and measurable. |

| AS 10 | Covers accounting for fixed assets, including acquisition, depreciation, and disposal of assets. |

| AS 11 | Deals with accounting for foreign exchange transactions and the impact of currency fluctuations. |

| AS 12 | Provides guidelines for accounting treatment of government grants and subsidies received by businesses. |

| AS 13 | Focuses on accounting for investments, including classification and valuation. |

Cost and Disclosure Standards

| Standard | Description |

| AS 15 | Covers employee benefits such as salaries, gratuity, and retirement benefits, ensuring proper expense recognition. |

| AS 16 | Deals with borrowing costs like interest and specifies when such costs should be capitalized or expensed. |

| AS 17 | Requires reporting of financial information based on different business segments for better analysis. |

| AS 18 | Ensures disclosure of transactions between related parties to maintain transparency. |

Advanced Standards

| Standard | Description |

| AS 19 | Covers accounting treatment for leases, distinguishing between operating and finance leases. |

| AS 20 | Defines calculation and reporting of earnings per share (EPS) for performance evaluation. |

| AS 21 | Deals with preparation of consolidated financial statements for group companies. |

| AS 22 | Focuses on accounting for income taxes, including deferred tax assets and liabilities. |

| AS 23 | Covers accounting for investments in associate companies using equity method. |

| AS 24 | Deals with reporting of discontinuing operations separately in financial statements. |

| AS 25 | Provides guidelines for preparing interim financial reports for shorter periods. |

Specialized Standards

| Standard | Description |

| AS 26 | Covers accounting for intangible assets such as goodwill, patents, and trademarks. |

| AS 27 | Deals with accounting for joint ventures and shared business arrangements. |

| AS 28 | Focuses on impairment of assets, ensuring assets are not carried above recoverable value. |

| AS 29 | Provides guidelines for provisions, contingent liabilities, and contingent assets. |

Withdrawn and Merged Standards

Understanding this helps avoid confusion when referring to outdated standards.

| Standard | Status |

| AS 6 | Merged into AS 10 (Depreciation now covered under fixed assets standard) |

| AS 30–32 | Withdrawn as they related to financial instruments |

AS vs Ind AS

India also follows Ind AS, which is aligned with international IFRS standards. However, applicability differs:

| Basis | AS (Indian GAAP) | Ind AS |

| Applicability | Small and medium businesses with simpler reporting needs | Large and listed companies |

| Complexity | Relatively simple and rule-based | More complex and principle-based |

| Usage | Widely used by SMEs | Mandatory for certain companies |

For most SMEs, Accounting Standards (AS) are sufficient.

Why Accounting Standards Matter

Even for small businesses, accounting standards play a crucial role in:

- Maintaining accurate financial records

- Ensuring tax and GST compliance

- Preparing for audits

- Improving financial decision-making

Check Out – How to Set Financial Goals for Your Small Business in 2026

Conclusion

Accounting Standards in India ensure consistency, accuracy, and compliance in financial reporting. While only a few standards are commonly used by small businesses, understanding them helps maintain proper records, avoid errors, and make better financial decisions. Using the right accounting tools can further simplify compliance and improve overall efficiency.